Ataxia Market Synopsis

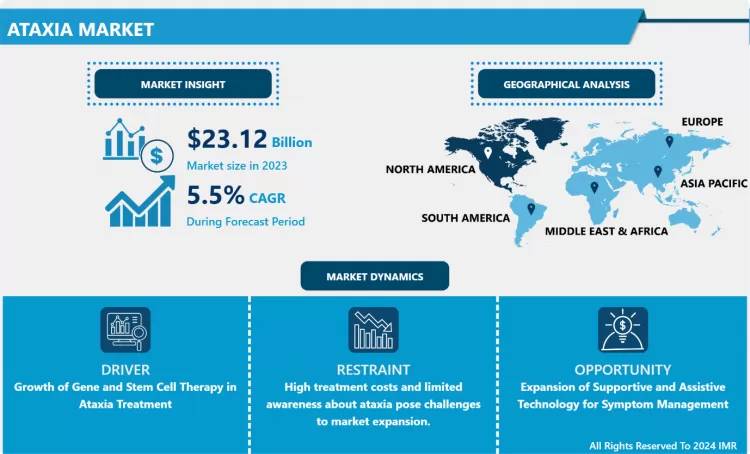

Ataxia Market Size Was Valued at USD 23.12 Billion in 2023 and is Projected to Reach USD 37.43 Billion by 2032, Growing at a CAGR of 5.50% From 2024-2032.

There is no cure for ataxia, supportive care products, diagnostics, and therapies used for treating the Ataxia market which is related to neurological disorders associated with stability and coordination along with speech impediment. There exist inherited ataxias, for instance, Friedreich’s ataxia and spinocerebellar ataxias, and acquired ataxias arising from factors including stroke, head trauma and infections hence making it a multipart system condition resulting from multiple causes with diverse manifestations. Rising knowledge and developments in genetics have affected this market by raising knowledge and diagnosis of the genetic forms of ataxia. In addition, there was growth in funding received by anxious researchers –thanks to which, understanding of the disease and new treatments has advanced.

- The biopharmaceutical sector and other pharmaceutical firms are fully engaged in the research of disease modifying therapies that analysts say will define the future of patient care. At the moment, the majority of ataxia therapies available to the market remain disease-modifying and are mainly designed to address complications such as, tremors, muscle spasms, and coordination problems. However there are certain good therapeutic approaches that are evolving as promising therapies for hereditary ataxias including gene therapy and stem cell therapy that is likely hold genetic abnormalities responsible for the condition. Such funding as government grants and support organizations have supported research and development making ataxia a focal area for new therapies in clinical trials.

- North American and European markets are the most active markets in ataxia research by being endowed with well developed health systems, dedicating higher percentage of their health budget on R and D, and by having favourable legislation on orphan drugs.s in the ataxia market are symptomatic, aiming to relieve issues like tremors, muscle spasms, and coordination challenges. However, gene therapy and stem cell therapy hold promise as emerging options that could potentially target the root causes of hereditary ataxias. Government grants, support organizations, and clinical trial networks have bolstered R&D efforts, making ataxia a high-priority area for new therapeutic exploration.

- The North American and European markets lead in ataxia research due to strong healthcare infrastructure, higher investment in orphan drug development, and supportive regulatory frameworks for rare diseases. However, the Asia-Pacific countries are still emerging markets providing slight signs of rising healthcare investments and escalating awareness. Based on increasing global incidence rates and enhanced diagnostic tools, the ataxia market is expected to develop gradually. There has also been advancement in industry collaborations, partnerships, and patient advocacy in an attempt to advance the development of affordable and effective ataxia treatments across the word.

Ataxia Market Trend Analysis

Growth of Gene and Stem Cell Therapy in Ataxia Treatment

- Ataxia: Gene and stem cell therapies are emerging as the value-added medicine for non-curable ataxias and promising approach to modulating the neurological aetiology of inherited ataxias. These therapies focus on a particular gene abnormality or put healthy cells in the brain to heal or as a substitute for the impaired neurons providing patients with an anticipated cure, rather than merely a cure of the signs and symptoms of the diseases. There are clinical trials for Friedreich’s ataxia and other hereditary forms of the disease are in progress in several biotechnology companies and research institutions, and preliminary studies suggest that further disease progression might be slowed, or even reversed. The tremendous spending and organisational support towards gene and stem cell therapies could soon reinvent ataxia management strategies.

Expansion of Supportive and Assistive Technology for Symptom Management

- Ataxia: Gene and stem cell therapies are emerging as the value-added medicine for non-curable ataxias and promising approach to modulating the neurological aetiology of inherited ataxias.. These therapies focus on a particular gene abnormality or put healthy cells in the brain to heal or as a substitute for the impaired neurons providing patients with an anticipated cure, rather than merely a cure of the signs and symptoms of the diseases. There are clinical trials for Friedreich’s ataxia and other hereditary forms of the disease are in progress in several biotechnology companies and research institutions, and preliminary studies suggest that further disease progression might be slowed, or even reversed. The tremendous spending and organisational support towards gene and stem cell therapies could soon reinvent ataxia management strategies.

Ataxia Market Segment Analysis:

Ataxia Market is Segmented on the basis of Type, Product, Dosage Form, Route of Administration, Patient Type, End User and Distribution Channel.

By Type, Spinocerebellar Ataxias segment is expected to dominate the market during the forecast period

- Ataxias can be broadly classified by type that are Spinocerebellar Ataxias, Ataxia-Telangiectasia, Episodic Ataxia and others including Multiple System Atrophy (MSA). Spinocerebellar ataxias comprise one of the largest groups of diseases because of their genetic basis and the myriad of subtypes, for which individual management strategies are necessary. Ataxia-Telangiectasia is a rare and complicated genetic disease, and this segment has early symptoms, so early treatment and the improvement of symptoms are main concerns. For example, Episodic Ataxia – the neurological disorder which might manifest as temporary loss of coordination – has different approaches to management as it seems to have triggers: stress, or physical activity. Lastly, conditions that come under “Others”, namely MSA, are progressive and the ataxia that affect multiple systems, the call for multidisciplinary treatment regimens in the emerging ataxia market.

By Distribution Channel, Direct Tender segment expected to held the largest share

- The following channels are used in the ataxia market namely direct tendering, retail and others to ensure that the consumers as well as institutions gain easier access to the medications, therapy as well as supportive equipments.. Many direct tenders focus on hospitals and specific treatment centres, so that such essential products and services can be provided to ataxia patients with severe or hard to treat forms of the disease. Retailing is also involved in the distribution of over-the-counter and prescription medicines, and relevant devices to individuals, through pharmacies and online. Other distribution channels, such as specialty suppliers and digitalhealth services, are also broadening and aligning themselves with disease-specific, patient-centered models of care that are making the suite of ataxia management solutions available to patients across various specialties and segments that are disparate to any one specialty area.

Ataxia Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America is likely to account for the largest market share in the ataxia market during the forecast period owing to well developed health care structure, high investment on neurological research and increasing number of clinical trials on ataxia treatment.. The area is also home to leading pharma/biotech companies that are committed to the discovery of new therapeutic approaches – gene and stem cell therapies targeted at hereditary ataxias included. In addition, both awareness and supportive policies have risen considerably, along with more efficient means of diagnosis, raising the rates of early diagnosis and intervention. This favorable environment places North American within strategic grounds when it comes to ataxia treatment and research.

Active Key Players in the Ataxia Market

- Novartis AG (Switzerland)

- Merck KGaA (Germany)

- Aurobindo Pharma (India)

- Pfizer Inc. (US)

- Sanofi (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Acorda Therapeutics, Inc. (US)

- Viatris Inc. (US)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin (India)

- Amneal Pharmaceuticals LLC (US)

- Apotex Inc. (Canada)

- Cipla Inc. (India)

- Biovista (US)

- Design Therapeutics Inc. (US)

- Reata Pharmaceuticals, Inc. (US)

- MATRIX BIOMED (US)

- Intrabio (UK)

- Biohaven Pharmaceuticals (US)

- Retrotope Inc. (US)

- Adverum Biotechnologies, Inc. (US)

- Priory (UK)

- Sutter Health (US)

- Upstream Rehabilitation Inc. (US)

- Banner Health (US)

- Select Medical Corporation (US)

- ATI Physical Therapy (US) and Other Major Players

|

Global Ataxia Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 23.12 Billion |

|

Forecast Period 2024-32 CAGR: |

5.50% |

Market Size in 2032: |

USD 37.43 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Dosage Form |

|

||

|

By Route of Administration |

|

||

|

Patient Type |

|

||

|

By End User |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Ataxia Market by By Type (2018-2032)

4.1 Ataxia Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Spinocerebellar Ataxias

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Ataxia-Telangiectasia

4.5 Episodic Ataxia

4.6 Others (Multiple System Atrophy (MSA))

Chapter 5: Ataxia Market by By Product (2018-2032)

5.1 Ataxia Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Treatment

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Diagnosis

Chapter 6: Ataxia Market by By Dosage Form (2018-2032)

6.1 Ataxia Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Solid

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Liquids

6.5 Others

Chapter 7: Ataxia Market by By Route of Administration (2018-2032)

7.1 Ataxia Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Oral

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Parenteral

7.5 Others

7.6 Patient Type

7.7 Adult

7.8 Child

7.9 Geriatric

Chapter 8: Ataxia Market by By End User (2018-2032)

8.1 Ataxia Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospital

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Clinics

8.5 Home Healthcare

8.6 Others

Chapter 9: Ataxia Market by By Distribution Channel (2018-2032)

9.1 Ataxia Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Direct Tender

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Retail Sales

9.5 Others

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Ataxia Market Share by Manufacturer (2024)

10.1.3 Industry BCG Matrix

10.1.4 Heat Map Analysis

10.1.5 Mergers and Acquisitions

10.2 NOVARTIS AG (SWITZERLAND)

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Key Strategic Moves and Recent Developments

10.2.10 SWOT Analysis

10.3 MERCK KGAA (GERMANY)

10.4 AUROBINDO PHARMA (INDIA)

10.5 PFIZER INC. (US)

10.6 SANOFI (FRANCE)

10.7 TEVA PHARMACEUTICAL INDUSTRIES LTD. (ISRAEL)

10.8 ACORDA THERAPEUTICS INC. (US)

10.9 VIATRIS INC. (US)

10.10 SUN PHARMACEUTICAL INDUSTRIES LTD. (INDIA)

10.11 LUPIN (INDIA)

10.12 AMNEAL PHARMACEUTICALS LLC (US)

10.13 APOTEX INC. (CANADA)

10.14 CIPLA INC. (INDIA)

10.15 BIOVISTA (US)

10.16 DESIGN THERAPEUTICS INC. (US)

10.17 REATA PHARMACEUTICALS INC. (US)

10.18 MATRIX BIOMED (US)

10.19 INTRABIO (UK)

10.20 BIOHAVEN PHARMACEUTICALS (US)

10.21 RETROTOPE INC. (US)

10.22 ADVERUM BIOTECHNOLOGIES INC. (US)

10.23 PRIORY (UK)

10.24 SUTTER HEALTH (US)

10.25 UPSTREAM REHABILITATION INC. (US)

10.26 BANNER HEALTH (US)

10.27 SELECT MEDICAL CORPORATION (US)

10.28 ATI PHYSICAL THERAPY (US)

Chapter 11: Global Ataxia Market By Region

11.1 Overview

11.2. North America Ataxia Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecasted Market Size By By Type

11.2.4.1 Spinocerebellar Ataxias

11.2.4.2 Ataxia-Telangiectasia

11.2.4.3 Episodic Ataxia

11.2.4.4 Others (Multiple System Atrophy (MSA))

11.2.5 Historic and Forecasted Market Size By By Product

11.2.5.1 Treatment

11.2.5.2 Diagnosis

11.2.6 Historic and Forecasted Market Size By By Dosage Form

11.2.6.1 Solid

11.2.6.2 Liquids

11.2.6.3 Others

11.2.7 Historic and Forecasted Market Size By By Route of Administration

11.2.7.1 Oral

11.2.7.2 Parenteral

11.2.7.3 Others

11.2.7.4 Patient Type

11.2.7.5 Adult

11.2.7.6 Child

11.2.7.7 Geriatric

11.2.8 Historic and Forecasted Market Size By By End User

11.2.8.1 Hospital

11.2.8.2 Clinics

11.2.8.3 Home Healthcare

11.2.8.4 Others

11.2.9 Historic and Forecasted Market Size By By Distribution Channel

11.2.9.1 Direct Tender

11.2.9.2 Retail Sales

11.2.9.3 Others

11.2.10 Historic and Forecast Market Size by Country

11.2.10.1 US

11.2.10.2 Canada

11.2.10.3 Mexico

11.3. Eastern Europe Ataxia Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecasted Market Size By By Type

11.3.4.1 Spinocerebellar Ataxias

11.3.4.2 Ataxia-Telangiectasia

11.3.4.3 Episodic Ataxia

11.3.4.4 Others (Multiple System Atrophy (MSA))

11.3.5 Historic and Forecasted Market Size By By Product

11.3.5.1 Treatment

11.3.5.2 Diagnosis

11.3.6 Historic and Forecasted Market Size By By Dosage Form

11.3.6.1 Solid

11.3.6.2 Liquids

11.3.6.3 Others

11.3.7 Historic and Forecasted Market Size By By Route of Administration

11.3.7.1 Oral

11.3.7.2 Parenteral

11.3.7.3 Others

11.3.7.4 Patient Type

11.3.7.5 Adult

11.3.7.6 Child

11.3.7.7 Geriatric

11.3.8 Historic and Forecasted Market Size By By End User

11.3.8.1 Hospital

11.3.8.2 Clinics

11.3.8.3 Home Healthcare

11.3.8.4 Others

11.3.9 Historic and Forecasted Market Size By By Distribution Channel

11.3.9.1 Direct Tender

11.3.9.2 Retail Sales

11.3.9.3 Others

11.3.10 Historic and Forecast Market Size by Country

11.3.10.1 Russia

11.3.10.2 Bulgaria

11.3.10.3 The Czech Republic

11.3.10.4 Hungary

11.3.10.5 Poland

11.3.10.6 Romania

11.3.10.7 Rest of Eastern Europe

11.4. Western Europe Ataxia Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecasted Market Size By By Type

11.4.4.1 Spinocerebellar Ataxias

11.4.4.2 Ataxia-Telangiectasia

11.4.4.3 Episodic Ataxia

11.4.4.4 Others (Multiple System Atrophy (MSA))

11.4.5 Historic and Forecasted Market Size By By Product

11.4.5.1 Treatment

11.4.5.2 Diagnosis

11.4.6 Historic and Forecasted Market Size By By Dosage Form

11.4.6.1 Solid

11.4.6.2 Liquids

11.4.6.3 Others

11.4.7 Historic and Forecasted Market Size By By Route of Administration

11.4.7.1 Oral

11.4.7.2 Parenteral

11.4.7.3 Others

11.4.7.4 Patient Type

11.4.7.5 Adult

11.4.7.6 Child

11.4.7.7 Geriatric

11.4.8 Historic and Forecasted Market Size By By End User

11.4.8.1 Hospital

11.4.8.2 Clinics

11.4.8.3 Home Healthcare

11.4.8.4 Others

11.4.9 Historic and Forecasted Market Size By By Distribution Channel

11.4.9.1 Direct Tender

11.4.9.2 Retail Sales

11.4.9.3 Others

11.4.10 Historic and Forecast Market Size by Country

11.4.10.1 Germany

11.4.10.2 UK

11.4.10.3 France

11.4.10.4 The Netherlands

11.4.10.5 Italy

11.4.10.6 Spain

11.4.10.7 Rest of Western Europe

11.5. Asia Pacific Ataxia Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecasted Market Size By By Type

11.5.4.1 Spinocerebellar Ataxias

11.5.4.2 Ataxia-Telangiectasia

11.5.4.3 Episodic Ataxia

11.5.4.4 Others (Multiple System Atrophy (MSA))

11.5.5 Historic and Forecasted Market Size By By Product

11.5.5.1 Treatment

11.5.5.2 Diagnosis

11.5.6 Historic and Forecasted Market Size By By Dosage Form

11.5.6.1 Solid

11.5.6.2 Liquids

11.5.6.3 Others

11.5.7 Historic and Forecasted Market Size By By Route of Administration

11.5.7.1 Oral

11.5.7.2 Parenteral

11.5.7.3 Others

11.5.7.4 Patient Type

11.5.7.5 Adult

11.5.7.6 Child

11.5.7.7 Geriatric

11.5.8 Historic and Forecasted Market Size By By End User

11.5.8.1 Hospital

11.5.8.2 Clinics

11.5.8.3 Home Healthcare

11.5.8.4 Others

11.5.9 Historic and Forecasted Market Size By By Distribution Channel

11.5.9.1 Direct Tender

11.5.9.2 Retail Sales

11.5.9.3 Others

11.5.10 Historic and Forecast Market Size by Country

11.5.10.1 China

11.5.10.2 India

11.5.10.3 Japan

11.5.10.4 South Korea

11.5.10.5 Malaysia

11.5.10.6 Thailand

11.5.10.7 Vietnam

11.5.10.8 The Philippines

11.5.10.9 Australia

11.5.10.10 New Zealand

11.5.10.11 Rest of APAC

11.6. Middle East & Africa Ataxia Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecasted Market Size By By Type

11.6.4.1 Spinocerebellar Ataxias

11.6.4.2 Ataxia-Telangiectasia

11.6.4.3 Episodic Ataxia

11.6.4.4 Others (Multiple System Atrophy (MSA))

11.6.5 Historic and Forecasted Market Size By By Product

11.6.5.1 Treatment

11.6.5.2 Diagnosis

11.6.6 Historic and Forecasted Market Size By By Dosage Form

11.6.6.1 Solid

11.6.6.2 Liquids

11.6.6.3 Others

11.6.7 Historic and Forecasted Market Size By By Route of Administration

11.6.7.1 Oral

11.6.7.2 Parenteral

11.6.7.3 Others

11.6.7.4 Patient Type

11.6.7.5 Adult

11.6.7.6 Child

11.6.7.7 Geriatric

11.6.8 Historic and Forecasted Market Size By By End User

11.6.8.1 Hospital

11.6.8.2 Clinics

11.6.8.3 Home Healthcare

11.6.8.4 Others

11.6.9 Historic and Forecasted Market Size By By Distribution Channel

11.6.9.1 Direct Tender

11.6.9.2 Retail Sales

11.6.9.3 Others

11.6.10 Historic and Forecast Market Size by Country

11.6.10.1 Turkiye

11.6.10.2 Bahrain

11.6.10.3 Kuwait

11.6.10.4 Saudi Arabia

11.6.10.5 Qatar

11.6.10.6 UAE

11.6.10.7 Israel

11.6.10.8 South Africa

11.7. South America Ataxia Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecasted Market Size By By Type

11.7.4.1 Spinocerebellar Ataxias

11.7.4.2 Ataxia-Telangiectasia

11.7.4.3 Episodic Ataxia

11.7.4.4 Others (Multiple System Atrophy (MSA))

11.7.5 Historic and Forecasted Market Size By By Product

11.7.5.1 Treatment

11.7.5.2 Diagnosis

11.7.6 Historic and Forecasted Market Size By By Dosage Form

11.7.6.1 Solid

11.7.6.2 Liquids

11.7.6.3 Others

11.7.7 Historic and Forecasted Market Size By By Route of Administration

11.7.7.1 Oral

11.7.7.2 Parenteral

11.7.7.3 Others

11.7.7.4 Patient Type

11.7.7.5 Adult

11.7.7.6 Child

11.7.7.7 Geriatric

11.7.8 Historic and Forecasted Market Size By By End User

11.7.8.1 Hospital

11.7.8.2 Clinics

11.7.8.3 Home Healthcare

11.7.8.4 Others

11.7.9 Historic and Forecasted Market Size By By Distribution Channel

11.7.9.1 Direct Tender

11.7.9.2 Retail Sales

11.7.9.3 Others

11.7.10 Historic and Forecast Market Size by Country

11.7.10.1 Brazil

11.7.10.2 Argentina

11.7.10.3 Rest of SA

Chapter 12 Analyst Viewpoint and Conclusion

12.1 Recommendations and Concluding Analysis

12.2 Potential Market Strategies

Chapter 13 Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

|

Global Ataxia Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 23.12 Billion |

|

Forecast Period 2024-32 CAGR: |

5.50% |

Market Size in 2032: |

USD 37.43 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Dosage Form |

|

||

|

By Route of Administration |

|

||

|

Patient Type |

|

||

|

By End User |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Ataxia Market research report is 2024-2032.

Novartis AG (Switzerland), Merck KGaA (Germany), Aurobindo Pharma (India), Pfizer Inc. (US), Sanofi (France), Teva Pharmaceutical Industries Ltd. (Israel), Acorda Therapeutics, Inc. (US), Viatris Inc. (US), Sun Pharmaceutical Industries Ltd. (India), Lupin (India), Amneal Pharmaceuticals LLC (US), Apotex Inc. (Canada), Cipla Inc. (India), Biovista (US), Design Therapeutics Inc. (US), Reata Pharmaceuticals, Inc. (US), MATRIX BIOMED (US), Intrabio (UK), Biohaven Pharmaceuticals (US), Retrotope Inc. (US), Adverum Biotechnologies, Inc. (US), Priory (UK), Sutter Health (US), Upstream Rehabilitation Inc. (US), Banner Health (US), Select Medical Corporation (US), ATI Physical Therapy (US), others.

The Ataxia Market is segmented into By Type, Product, Dosage Form, Route of Administration, Patient Type, End User, By Distribution Channel and region. By Type (Spinocerebellar Ataxias, Ataxia-Telangiectasia, Episodic Ataxia, and Others (Multiple System Atrophy (MSA))), Product (Treatment and Diagnosis), Dosage Form (Solid, Liquids, and Others), Route of Administration (Oral, Parenteral, and Others), Patient Type (Adult, Child, and Geriatric), End User (Hospital, Clinics, Home Healthcare, and Others), Distribution Channel (Direct Tender, Retail Sales, and Others). By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

There are no cure for ataxia, supportive care products, diagnostics, and therapies used for treating Ataxia market which is related to neurological disorders associated with stability and coordination along with speech impediment. There exist inherited ataxias, for instance, Friedreich’s ataxia and spinocerebellar ataxias, and acquired ataxias arising from factors including stroke, head trauma and infections hence making it a multipart system condition resulting from multiple causes with diverse manifestations. Rising knowledge and developments in genetics have affected this market by raising knowledge and diagnosis of the genetic forms of ataxia. In addition, there was growth in funding received by anxious researchers –thanks to which, understanding of the disease and new treatments has advanced.

Ataxia Market Size Was Valued at USD 23.12 Billion in 2023 and is Projected to Reach USD 37.43 Billion by 2032, Growing at a CAGR of 5.50% From 2024-2032.