Cardiovascular Ultrasound Market Synopsis:

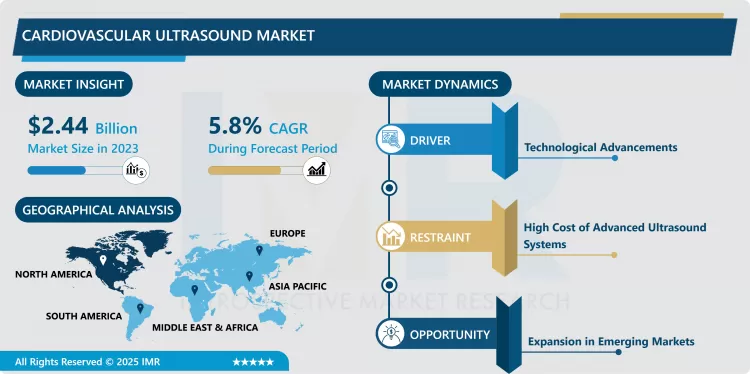

Cardiovascular Ultrasound Market Size Was Valued at USD 2.44 Billion in 2023, and is Projected to Reach USD 4.05 Billion by 2032, Growing at a CAGR of 5.80% From 2024-2032.

The cardiovascular ultrasound market refers to the global market of producing, manufacturing, and supplying ultrasound imaging therapies for assessing and diagnosing cardiovascular diseases. Various modalities prevalence applies to this market include; echocardiography, Doppler ultrasound, and an advanced tool such as three-dimensional imaging used by healthcare practitioners to evaluate heart function, blood flow, and vascular pathology without surgery. Heart disorders are on the rise, imaging techniques are improving, and there is emphasis placed on diagnostics and prevention leading to the need for cardiovascular ultrasound systems. This is why the given market is an important contributing factor in improving the patient’s outcomes and contributing to effective treatment in cardiology.

Currently, the global cardiovascular ultrasound market has grown rapidly due to changing awareness on CVDs and development of ultrasound technology. Cardiovascular diseases continue to influence high morbidity and mortality rates worldwide, and hence the need for effective diagnostic methods. Of all imaging methods, ultrasound imaging, especially echocardiography are preferred because they are non invasive; provide real time images and is relatively cheaper. More advanced technologies include 3D echocardiography, portable ultrasound devices which in addition to AI improves the cardiovascular diagnostic accuracy and makes them available to other physicians.

Regionally, North America is expected to maintain high market growth in the cardiovascular ultrasound market due to factors such as increased health care spending, advanced health care facilities and aumento di una popolazione invecchiata suscettibile a malattie cardiache. Europe is also experiencing considerable growth due to the enhanced healthcare sector investment in technologies, as well efforts to cope with new lifestyle diseases. However, Asia-Pacific area is proving to be a vast market, with newly developing and highly developed health care system, fast increasing standards of living, and increasing concerns to prevent rather than cure. The increase in risk factors that include obesity, hypertension and diabetes in developing economic zones, will further spur the need for cardiovascular ultrasound services.

the market is quite saturated here and some of the companies are trying to capture more market by forming strategic alliances, mergers and acquisitions. Further advancements in ultrasound technology is necessary for provision of new imaging software, as well as mobility solutions for doctors’ requirements in their practice. Moreover, the ever-growing pattern of telecardiology and home-monitoring is going to enhances the implementation of cardiovascular ultrasound systems even in the rural and low-resource regions. In total, the cardiovascular ultrasound market is expected to experience further growth owing to the advanced technology, higher disease incidence, and changing priorities towards diagnosing and preventing cardiovascular diseases.

Cardiovascular Ultrasound Market Trend Analysis:

The Role of AI and Accessibility Innovations

- One can say that the incorporation of artificial intelligence AI into ultrasound devices is greatly reshaping the cardiovascular ultrasound market mainly due to the improvement of the image quality and the subsequent increase in accuracy of the diagnostics performed. Healthcare providers are now able to diagnose cardiovascular diseases with greater efficiency and accuracy through use of AI algorithms meant to analyze real-time images. Some of the benefits of this development include an increased ability to minimize human interventions thereby increasing accuracy in the ultrasound image interpretations. This is why health care persons can pick up early signs of defects, valve malfunctions, coronary diseases etc, and provide intervention early thus better patient outcomes.

- Moreover, advances in the compact and handheld ultrasound machines are increasing the cardiovascular imaging overview and its availability in regions with limited or no stationary imaging technology. These are small devices that enable people to take screenings in homes, community-based facilities, and for emergencies. The global rise in the understanding of cardiovascular diseases, and the shift towards disease prevention, are influencing the usage of ultrasound technologies not only in clinical situations but also in home care contexts as well. Growing awareness of the early diagnosis and regular monitoring concepts by both patients and providers will create additional interest in accessible, easy-to-use ultrasound solutions, thus driving the market forward.

The Growing Demand for Cardiovascular Ultrasound in Disease Management

- CVDs are currently the number one killer world over and hence the need for practical diagnostic tools for early detection of these ailments. Of these tools, cardiovascular ultrasound, especially echocardiography, is an essential modality overly because it is non invasive and cheap for clinicians. The Echo GOAL is calculated from the radial arterial waveform obtained from the finger systolic pressure waveform, and the software displays images and values in real-time. This technology gives information about the cardiac structure and function in real time making diagnosis of diseases quicker and accurate. In this case, the increased diagnostic ability is crucial in creating specific treatment regimens based on patients’ specifics in an attempt to enhance patient care and management of the CVDs burden.

- Moreover, adhesive change to preventive health has promoted the use of cardiovascular ultrasound among people. Healthcare providers have embraced the use of ultrasound technology during examinations especially focusing on the heart we add health. This goes a long way into preventive cardiovascular sign observation apart from putting the patient in charge of his/her cardiovascular health. In addition to the improvements in identifiable ultrasound, such as mobile devices and additional options, more clients can be reached by doctors, especially those in more distant locations. Therefore, cardiovascular ultrasound market has great prospects in progress, due to the increasing tendencies towards preventive treatment and the availability of diagnostic systems at the management of cardiovascular pathologies.

Cardiovascular Ultrasound Market Segment Analysis:

Cardiovascular Ultrasound Market is Segmented on the basis of Type, Technology, Display, End-use, and Region

By Type, Transthoracic echocardiography segment is expected to dominate the market during the forecast period

- TTE is the most common type of echocardiography being known for its non-intrusive modality and ability to capture important information regarding the condition of a patient’s heart. When the transducer is placed on the chest wall in contact with the skin, real-time images of the heart can be ascertained, which give an impression of its size as well as structure and function. TTE is used in the identification of several heart conditions; valve disorders, heart muscle disorders, and even congenital disorders. Its capability implies that it is the primary instrument for diagnosing patients with cardiovascular complaints as it admits the opportunity to timely treat heart diseases.

- Cardiovascular diseases are on the rise, and the global population requires TTE more as the doctors look for ways to perform regular and emergency check-ups. Ultrasound has also progressed over the recent past to increase the efficiency of TTE offering better images to analyse. Also, since TTE can be carried out in hospitals inpatients, outpatient clinics, and even at the bedside, it is well placed in current cardiovascular practice. With the growth in awareness of heart health and an ageing population, TTE will retain its role of a valuable tool in echocardiography for the diagnosis of cardio vascular diseases, improved treatment through early intervention.

By End-use, Hospital segment expected to held the largest share

- Cardiac departments in hospitals hold the biggest demand for echocardiography devices, due to the broad variety of echocardiography applications in practically every section of a busy hospital that serves both inpatient and outpatient needs. The main offices are endowed with high end echocardiography systems that include 2D, 3D and Doppler systems. The incorporation of these complex systems in cardiac care units improves the capacity for real time assessment of the underlying problems affecting the heart and makes it easier to make sound decisions on a course of treatment. When diagnosis and treatment of diseases is the goal of every hospital today, then it is imperative that the latest innovative technology in echocardiography devices is employed in cardiovascular management.

- Hospitals have seen a rise in demand in developing nations due to the rising incidence of cardiovascular diseases, in the global market. Caucasian population is aging, and more people develop other lifestyle risk factors, so efficient interventions and diagnostics have never been as important. There has been a rise in echocardiography utilization because hospitals have an emphasis on the efficiency of cardiac services. To this end, the demand for wide range diagnostic services in cardiology practices that must be able to accommodate a high patient traffic make echocardiography a core service delivery modality within the field. So, over the time, the diverse advancements in the new technologies and the improvements in the cardiac care services among the hospitals make the hospital-based echocardiography market to have the potential to grow in near future.

Cardiovascular Ultrasound Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- The cardiovascular ultrasound market in North American, specially the United States, is well established as the region has first-hand information about the dangers of cardiovascular diseases affecting the population. Demographics and the increasing prevalence of health issues including an aging population, elevated BMI and other diseases such as hypertension and diabetes all contribute to this need. The Region has a well-developed health care system where cardiovascular ultrasound is an essential diagnostic tool for early diagnosis and management of heart diseases. Due to the good healthcare funding system and quality medical practice, these ultrasound devices are widely used, and it improves the patients’ status and ensures the market’s further development.

- Moreover, the United States enjoys a robust primary care focus, whereby the clinicians devote considerable time recognising and controlling the factors that contribute to cardiovascular diseases. This approach is complemented by the increasing population’s consciousness of the necessity to check one’s cardiovascular profile and get checked up. Besides, the key market players are a part of this region, which endorses competitiveness and innovation in imaging technologies and provides improved ultrasound devices. Major cardiovascular ultrasound devices are used by various independent practitioners, clinics, and hospitals to provide healthier working and more accurate diagnostic instruments, and as healthcare professional embrace these sophisticated tools they will definitely require them to provide appropriate efficient cardiovascular treatments that will positively support the growth trajectory of the North American cardiovascular ultrasound device market.

Active Key Players in the Cardiovascular Ultrasound Market:

- Koninklijke Philips N.V.

- GE Healthcare

- Siemens Healthineers AG

- Canon Medical Systems

- Mindray Medical International Limited

- Samsung Medison Co., Ltd.

- FUJIFILM SonoSite, Inc.,

- Konica Minolta Inc.

- Esaote

- Trivitron Healthcare

- Other Active Players

|

Cardiovascular Ultrasound Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.44 Billion |

|

Forecast Period 2024-32 CAGR: |

5.80% |

Market Size in 2032: |

USD 4.05 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Technology |

|

||

|

By Display |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Cardiovascular Ultrasound Market by By Type (2018-2032)

4.1 Cardiovascular Ultrasound Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Transthoracic echocardiography

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Transesophageal echocardiography

4.5 Fetal echocardiography

4.6 Others

Chapter 5: Cardiovascular Ultrasound Market by By Technology (2018-2032)

5.1 Cardiovascular Ultrasound Market Snapshot and Growth Engine

5.2 Market Overview

5.3 2D

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 3D/4D

5.5 Doppler

Chapter 6: Cardiovascular Ultrasound Market by By Display (2018-2032)

6.1 Cardiovascular Ultrasound Market Snapshot and Growth Engine

6.2 Market Overview

6.3 B/W

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Color

Chapter 7: Cardiovascular Ultrasound Market by By End-use (2018-2032)

7.1 Cardiovascular Ultrasound Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospital

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Diagnostic centers

7.5 Ambulatory care centers

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Cardiovascular Ultrasound Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 KONINKLIJKE PHILIPS N.V.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 GE HEALTHCARE

8.4 SIEMENS HEALTHINEERS AG

8.5 CANON MEDICAL SYSTEMS

8.6 MINDRAY MEDICAL INTERNATIONAL LIMITED

8.7 SAMSUNG MEDISON CO. LTD.

8.8 FUJIFILM SONOSITE INC.

8.9 KONICA MINOLTA INC.

8.10 ESAOTE

8.11 TRIVITRON HEALTHCARE

8.12 OTHER ACTIVE PLAYERS

Chapter 9: Global Cardiovascular Ultrasound Market By Region

9.1 Overview

9.2. North America Cardiovascular Ultrasound Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size By By Type

9.2.4.1 Transthoracic echocardiography

9.2.4.2 Transesophageal echocardiography

9.2.4.3 Fetal echocardiography

9.2.4.4 Others

9.2.5 Historic and Forecasted Market Size By By Technology

9.2.5.1 2D

9.2.5.2 3D/4D

9.2.5.3 Doppler

9.2.6 Historic and Forecasted Market Size By By Display

9.2.6.1 B/W

9.2.6.2 Color

9.2.7 Historic and Forecasted Market Size By By End-use

9.2.7.1 Hospital

9.2.7.2 Diagnostic centers

9.2.7.3 Ambulatory care centers

9.2.7.4 Others

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Cardiovascular Ultrasound Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size By By Type

9.3.4.1 Transthoracic echocardiography

9.3.4.2 Transesophageal echocardiography

9.3.4.3 Fetal echocardiography

9.3.4.4 Others

9.3.5 Historic and Forecasted Market Size By By Technology

9.3.5.1 2D

9.3.5.2 3D/4D

9.3.5.3 Doppler

9.3.6 Historic and Forecasted Market Size By By Display

9.3.6.1 B/W

9.3.6.2 Color

9.3.7 Historic and Forecasted Market Size By By End-use

9.3.7.1 Hospital

9.3.7.2 Diagnostic centers

9.3.7.3 Ambulatory care centers

9.3.7.4 Others

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Cardiovascular Ultrasound Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size By By Type

9.4.4.1 Transthoracic echocardiography

9.4.4.2 Transesophageal echocardiography

9.4.4.3 Fetal echocardiography

9.4.4.4 Others

9.4.5 Historic and Forecasted Market Size By By Technology

9.4.5.1 2D

9.4.5.2 3D/4D

9.4.5.3 Doppler

9.4.6 Historic and Forecasted Market Size By By Display

9.4.6.1 B/W

9.4.6.2 Color

9.4.7 Historic and Forecasted Market Size By By End-use

9.4.7.1 Hospital

9.4.7.2 Diagnostic centers

9.4.7.3 Ambulatory care centers

9.4.7.4 Others

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Cardiovascular Ultrasound Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size By By Type

9.5.4.1 Transthoracic echocardiography

9.5.4.2 Transesophageal echocardiography

9.5.4.3 Fetal echocardiography

9.5.4.4 Others

9.5.5 Historic and Forecasted Market Size By By Technology

9.5.5.1 2D

9.5.5.2 3D/4D

9.5.5.3 Doppler

9.5.6 Historic and Forecasted Market Size By By Display

9.5.6.1 B/W

9.5.6.2 Color

9.5.7 Historic and Forecasted Market Size By By End-use

9.5.7.1 Hospital

9.5.7.2 Diagnostic centers

9.5.7.3 Ambulatory care centers

9.5.7.4 Others

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Cardiovascular Ultrasound Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size By By Type

9.6.4.1 Transthoracic echocardiography

9.6.4.2 Transesophageal echocardiography

9.6.4.3 Fetal echocardiography

9.6.4.4 Others

9.6.5 Historic and Forecasted Market Size By By Technology

9.6.5.1 2D

9.6.5.2 3D/4D

9.6.5.3 Doppler

9.6.6 Historic and Forecasted Market Size By By Display

9.6.6.1 B/W

9.6.6.2 Color

9.6.7 Historic and Forecasted Market Size By By End-use

9.6.7.1 Hospital

9.6.7.2 Diagnostic centers

9.6.7.3 Ambulatory care centers

9.6.7.4 Others

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Cardiovascular Ultrasound Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size By By Type

9.7.4.1 Transthoracic echocardiography

9.7.4.2 Transesophageal echocardiography

9.7.4.3 Fetal echocardiography

9.7.4.4 Others

9.7.5 Historic and Forecasted Market Size By By Technology

9.7.5.1 2D

9.7.5.2 3D/4D

9.7.5.3 Doppler

9.7.6 Historic and Forecasted Market Size By By Display

9.7.6.1 B/W

9.7.6.2 Color

9.7.7 Historic and Forecasted Market Size By By End-use

9.7.7.1 Hospital

9.7.7.2 Diagnostic centers

9.7.7.3 Ambulatory care centers

9.7.7.4 Others

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Cardiovascular Ultrasound Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.44 Billion |

|

Forecast Period 2024-32 CAGR: |

5.80% |

Market Size in 2032: |

USD 4.05 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Technology |

|

||

|

By Display |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Cardiovascular Ultrasound Market research report is 2024-2032.

Koninklijke Philips N.V.; GE Healthcare; Siemens Healthineers AG; Canon Medical Systems; Mindray Medical International Limited; Samsung Medison Co., Ltd.; FUJIFILM SonoSite, Inc.; Konica Minolta Inc.; Esaote, Trivitron Healthcare and Other Active Players.

The Cardiovascular Ultrasound Market is segmented into By Type, By Technology, By Display, By End-use and region. By Type, the market is categorized into Transthoracic echocardiography, Transesophageal echocardiography, Fetal echocardiography and Others. By Technology, the market is categorized into 2D, 3D/4D, Doppler. By Display, the market is categorized into B/W and Color. By End-use, the market is categorized into Hospital, Diagnostic centers, Ambulatory care centers and Others. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, The Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC), Middle East & Africa (Turkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil, Argentina, Rest of SA).

The cardiovascular ultrasound market encompasses the development, manufacturing, and distribution of ultrasound imaging devices specifically designed for evaluating and diagnosing cardiovascular conditions. This market includes various modalities such as echocardiography, Doppler ultrasound, and three-dimensional imaging, which enable healthcare professionals to assess heart function, blood flow, and vascular abnormalities in a non-invasive manner. The increasing prevalence of cardiovascular diseases, advancements in imaging technology, and the growing emphasis on early diagnosis and preventive care drive the demand for cardiovascular ultrasound systems. As a result, this market plays a critical role in enhancing patient outcomes and facilitating effective treatment strategies in cardiology.

Cardiovascular Ultrasound Market Size Was Valued at USD 2.44 Billion in 2023, and is Projected to Reach USD 4.05 Billion by 2032, Growing at a CAGR of 5.80% From 2024-2032.