Drug Delivery Device Market Synopsis:

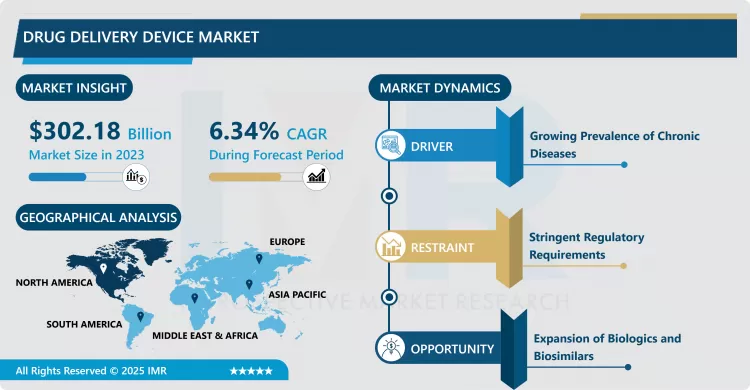

Drug Delivery Device Market Size Was Valued at USD 302.18 Billion in 2023, and is Projected to Reach USD 31.50 Billion by 2032, Growing at a CAGR of 6.34% From 2024-2032.

The drug delivery device market comprises tools and technologies that are applied to deliver therapeutic agents to a patient in a controlled, efficient manner. Products include syringes, inhalers, transdermal patches, amongst many others; each product has helped facilitate targeted effective delivery of the medication. Product development is guided by the demand for enhanced patient outcomes, the reduction of side effects, and the optimization of bioavailability of drugs.

The drug delivery device market is quite an important field under the larger umbrella of healthcare as this focus area contributes to the development and innovation in designing devices that deliver drugs with high accuracy and convenience. The value for such devices lies in improving treatment adherence, especially in chronic diseases such as diabetes, cardiovascular conditions, and respiratory ailments. Through the advancement of years, drug delivery devices have been transformed to be more patient-friendly, providing self-administration opportunities with fewer clinical interventions. This is on top of the prioritized changes at this point in time, not only for reasons of increasing the cost of healthcare but for home-based treatments as an alternative or replacement for clinical visits.

Among current innovations driving market progress are smart drug delivery systems and wearable injectors. These devices are designed to provide real-time monitoring, controlled release, and accurate dosing, thereby enhancing therapeutic effectiveness. Meanwhile, chronic diseases continue to rise in prevalence and age trends do not seem to show signs of decline, while demand for less invasive treatments continues to drive the level of this market forward. Moreover, regulatory authorities have helped create the conditions by legislating new drug-device combination products that help enhance patient compliance and quality of life. These trends put the market on a healthy growth track.

Drug Delivery Device Market Trend Analysis:

Rise of Smart Drug Delivery Devices

- It is the trend about smart drug delivery devices. It involves integration of health care solutions with advancing technologies to improve delivery of drugs. Such a device is advanced technology in the sense that, it integrates sensors and digital interfaces. Which allows patients and healthcare workers to follow real-time updates of the progression of treatment, adherence, and efficacy of the drug given. This is very helpful for chronic diseases, which requires effective and consistent dosing.

- Integration of AI and IoT in drug delivery devices brings the revolution in healthcare by providing personalized approaches to treatment. Smart devices can notify adjustments to therapy based on patterns found in patient behavior through data-driven insight. This really is in line with the emphasis put on the shift toward personalized medicine and preventive healthcare, where optimum treatments are ensured with minimal effects on the patients.

Expansion of Biologics and Biosimilars

- The rising demand for biologics and biosimilars is a great promise in the arena of drug delivery devices. Biologic drugs are high molecular mass, hence huge and sensitive in nature, which mandates greater innovative delivery solutions. Several devices have been developed for safe delivery that will provide safety along with patient comfort and convenience-from autoinjectors and prefilled syringes to wearable injectors.

- As the biosimilars market expands, delivery devices will be needed to be efficient and friendly to the patient. Increased approval of biosimilars by regulatory authorities, such as the FDA and EMA, further opens this space for cheaper treatment therapies in chronic diseases like cancer, diabetes, and autoimmune disorders. In the wake of such trends, drug delivery companies are trying to take advantage of this and improve by designing different products catering specifically to the unique needs of biologic and biosimilar administration.

Drug Delivery Device Market Segment Analysis:

Drug Delivery Device Market is Segmented on the basis of Route of Administration, application, end user, and region

By Route of Administration, Oral segment is expected to dominate the market during the forecast period

- The market for drug delivery devices is segmented into several types of routes of administration, such as oral, inhalation, transdermal, injectable, ocular, nasal, topical, and others. Oral is the most common and patient-friendly route of administration, easy to use with minimum invasiveness. Improved designs for drugs through devices such as oral dispersible tablets and controlled-release formulations have increased efficacy and compliance among patients. However, it often does not apply to biologics and large-molecule drugs, which require other solutions.

- Inhalation and injectable routes are getting popularity during the last few years mainly in chronic diseases such as asthma, diabetes, and autoimmune disorders. The route of inhalation is very generally most used for respiratory diseases, whereas the injectable route is preferred for biologics, insulin, and vaccines. The wearable injector and autoinjector are gaining popularity because patients can directly inject their drug on their own, and these routes are getting more attractive.

By Application, Oncology segment expected to held the largest share

- Therapeutic areas Drug delivery devices cover oncology, infectious disease, respiratory diseases, diabetes, cardiovascular diseases, autoimmune diseases, central nervous system disorders, as well as many other diseases. Oncology is a huge segment because, in recent years, there has been an increase in cases of cancer over the world and the need for accurate therapies. Infusion pumps and implantable systems are the most commonly used delivery modes for chemotherapy and other treatments to the cancer patient.

- The other major application area is diabetes, primarily boosted by the increase in global burden of disease. Devices such as the insulin pen, pump, and continuous glucose monitor largely improved the management of diabetes through more comfortability and precision in drug delivery. Other chronic diseases include respiratory disorders and cardiovascular diseases; these chronic diseases also have advanced methods of delivery for longer-term therapy, hence improving patient outcomes and lowering health care expenditures.

Drug Delivery Device Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America occupies the largest share in the global drug delivery device market. The advanced healthcare infrastructure, high adoption of novel medical technology, and strength in pharmaceuticals and biotechnology are some major reasons for this supremacy. North America contains the largest market for drug delivery devices, with big investment in research and development, a conducive regulatory environment, and increased demand from patients to get self-administered treatments.

- The region has a high incidence of chronic diseases, and there is a growing emphasis on home health care, which has upped the requirement for sophisticated drug delivery devices. A strong presence of key market players coupled with an established distribution network remains the most critical drivers of North America's leading position in the world drug delivery device market.

Active Key Players in the Drug Delivery Device Market:

- Becton, Dickinson and Company (USA)

- Medtronic plc (Ireland)

- Johnson & Johnson (USA)

- Gerresheimer AG (Germany)

- Ypsomed Holding AG (Switzerland)

- West Pharmaceutical Services, Inc. (USA)

- Novo Nordisk A/S (Denmark)

- 3M Company (USA)

- Pfizer, Inc. (USA)

- Bayer AG (Germany)

- GlaxoSmithKline plc (UK)

- Sanofi S.A. (France)

- Other Active Players

Key Industry Developments in the Drug Delivery Device Market:

- February 2023: Innovation Zed, one of the leading key players, received the CE mark for its InsulCheck DOSE, a single-unit add-on device for insulin pen injectors.

- September 2022: Corium, Inc., a biopharmaceutical company, launched ADLARITY, a donepezil transdermal system in the U.S. for treating patients suffering from mild to severe Alzheimer’s.

- August 2022: Baxter announced the U.S. FDA Clearance of the Novum IQ Syringe Infusion Pump with Dose IQ Safety Software. The Novum IQ Syringe infusion pumps precisely deliver small amounts of fluid at low rates, frequently in pediatric, neonatal or anesthesia care settings.

- June 2022: Gufic Biosciences Ltd launched a new drug delivery system, dual-chamber bags, in India. These dual-chamber IV bags are made of polypropylene with peelable aluminum foil, allowing the storage of unstable drugs that need reconstitution just before their administration to the patient.

- March 2022: Vitaris, Inc., in partnership with Kindeva Drug Delivery L.P., received the U.S. FDA approval for Breyna, a drug-device inhalation aerosol combination for patients suffering from asthma and COPD.

|

Drug Delivery Device Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 302.18 Billion |

|

Forecast Period 2024-32 CAGR: |

6.34% |

Market Size in 2032: |

USD 31.50 Billion |

|

Segments Covered: |

By Route of Administration |

|

|

|

By Application |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Drug Delivery Device Market by By Route of Administration (2018-2032)

4.1 Drug Delivery Device Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Oral

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Inhalation

4.5 Transdermal

4.6 Injectable

4.7 Ocular

4.8 Nasal

4.9 Topical

4.10 Others

Chapter 5: Drug Delivery Device Market by By Application (2018-2032)

5.1 Drug Delivery Device Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Oncology

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Infectious Diseases

5.5 Respiratory Diseases

5.6 Diabetes

5.7 Cardiovascular Diseases

5.8 Autoimmune Diseases

5.9 Central Nervous System Disorders

5.10 Others

Chapter 6: Drug Delivery Device Market by By End-use (2018-2032)

6.1 Drug Delivery Device Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Diagnostic Centers

6.5 Ambulatory Surgery Centers/Clinics

6.6 Home Care Settings

6.7 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Drug Delivery Device Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 BECTON

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 DICKINSON AND COMPANY (USA)

7.4 MEDTRONIC PLC (IRELAND)

7.5 JOHNSON & JOHNSON (USA)

7.6 GERRESHEIMER AG (GERMANY)

7.7 YPSOMED HOLDING AG (SWITZERLAND)

7.8 WEST PHARMACEUTICAL SERVICES INC. (USA)

7.9 NOVO NORDISK A/S (DENMARK)

7.10 3M COMPANY (USA)

7.11 OTHER ACTIVE PLAYERS

Chapter 8: Global Drug Delivery Device Market By Region

8.1 Overview

8.2. North America Drug Delivery Device Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By By Route of Administration

8.2.4.1 Oral

8.2.4.2 Inhalation

8.2.4.3 Transdermal

8.2.4.4 Injectable

8.2.4.5 Ocular

8.2.4.6 Nasal

8.2.4.7 Topical

8.2.4.8 Others

8.2.5 Historic and Forecasted Market Size By By Application

8.2.5.1 Oncology

8.2.5.2 Infectious Diseases

8.2.5.3 Respiratory Diseases

8.2.5.4 Diabetes

8.2.5.5 Cardiovascular Diseases

8.2.5.6 Autoimmune Diseases

8.2.5.7 Central Nervous System Disorders

8.2.5.8 Others

8.2.6 Historic and Forecasted Market Size By By End-use

8.2.6.1 Hospitals

8.2.6.2 Diagnostic Centers

8.2.6.3 Ambulatory Surgery Centers/Clinics

8.2.6.4 Home Care Settings

8.2.6.5 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Drug Delivery Device Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By By Route of Administration

8.3.4.1 Oral

8.3.4.2 Inhalation

8.3.4.3 Transdermal

8.3.4.4 Injectable

8.3.4.5 Ocular

8.3.4.6 Nasal

8.3.4.7 Topical

8.3.4.8 Others

8.3.5 Historic and Forecasted Market Size By By Application

8.3.5.1 Oncology

8.3.5.2 Infectious Diseases

8.3.5.3 Respiratory Diseases

8.3.5.4 Diabetes

8.3.5.5 Cardiovascular Diseases

8.3.5.6 Autoimmune Diseases

8.3.5.7 Central Nervous System Disorders

8.3.5.8 Others

8.3.6 Historic and Forecasted Market Size By By End-use

8.3.6.1 Hospitals

8.3.6.2 Diagnostic Centers

8.3.6.3 Ambulatory Surgery Centers/Clinics

8.3.6.4 Home Care Settings

8.3.6.5 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Drug Delivery Device Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By By Route of Administration

8.4.4.1 Oral

8.4.4.2 Inhalation

8.4.4.3 Transdermal

8.4.4.4 Injectable

8.4.4.5 Ocular

8.4.4.6 Nasal

8.4.4.7 Topical

8.4.4.8 Others

8.4.5 Historic and Forecasted Market Size By By Application

8.4.5.1 Oncology

8.4.5.2 Infectious Diseases

8.4.5.3 Respiratory Diseases

8.4.5.4 Diabetes

8.4.5.5 Cardiovascular Diseases

8.4.5.6 Autoimmune Diseases

8.4.5.7 Central Nervous System Disorders

8.4.5.8 Others

8.4.6 Historic and Forecasted Market Size By By End-use

8.4.6.1 Hospitals

8.4.6.2 Diagnostic Centers

8.4.6.3 Ambulatory Surgery Centers/Clinics

8.4.6.4 Home Care Settings

8.4.6.5 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Drug Delivery Device Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By By Route of Administration

8.5.4.1 Oral

8.5.4.2 Inhalation

8.5.4.3 Transdermal

8.5.4.4 Injectable

8.5.4.5 Ocular

8.5.4.6 Nasal

8.5.4.7 Topical

8.5.4.8 Others

8.5.5 Historic and Forecasted Market Size By By Application

8.5.5.1 Oncology

8.5.5.2 Infectious Diseases

8.5.5.3 Respiratory Diseases

8.5.5.4 Diabetes

8.5.5.5 Cardiovascular Diseases

8.5.5.6 Autoimmune Diseases

8.5.5.7 Central Nervous System Disorders

8.5.5.8 Others

8.5.6 Historic and Forecasted Market Size By By End-use

8.5.6.1 Hospitals

8.5.6.2 Diagnostic Centers

8.5.6.3 Ambulatory Surgery Centers/Clinics

8.5.6.4 Home Care Settings

8.5.6.5 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Drug Delivery Device Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By By Route of Administration

8.6.4.1 Oral

8.6.4.2 Inhalation

8.6.4.3 Transdermal

8.6.4.4 Injectable

8.6.4.5 Ocular

8.6.4.6 Nasal

8.6.4.7 Topical

8.6.4.8 Others

8.6.5 Historic and Forecasted Market Size By By Application

8.6.5.1 Oncology

8.6.5.2 Infectious Diseases

8.6.5.3 Respiratory Diseases

8.6.5.4 Diabetes

8.6.5.5 Cardiovascular Diseases

8.6.5.6 Autoimmune Diseases

8.6.5.7 Central Nervous System Disorders

8.6.5.8 Others

8.6.6 Historic and Forecasted Market Size By By End-use

8.6.6.1 Hospitals

8.6.6.2 Diagnostic Centers

8.6.6.3 Ambulatory Surgery Centers/Clinics

8.6.6.4 Home Care Settings

8.6.6.5 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Drug Delivery Device Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By By Route of Administration

8.7.4.1 Oral

8.7.4.2 Inhalation

8.7.4.3 Transdermal

8.7.4.4 Injectable

8.7.4.5 Ocular

8.7.4.6 Nasal

8.7.4.7 Topical

8.7.4.8 Others

8.7.5 Historic and Forecasted Market Size By By Application

8.7.5.1 Oncology

8.7.5.2 Infectious Diseases

8.7.5.3 Respiratory Diseases

8.7.5.4 Diabetes

8.7.5.5 Cardiovascular Diseases

8.7.5.6 Autoimmune Diseases

8.7.5.7 Central Nervous System Disorders

8.7.5.8 Others

8.7.6 Historic and Forecasted Market Size By By End-use

8.7.6.1 Hospitals

8.7.6.2 Diagnostic Centers

8.7.6.3 Ambulatory Surgery Centers/Clinics

8.7.6.4 Home Care Settings

8.7.6.5 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Drug Delivery Device Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 302.18 Billion |

|

Forecast Period 2024-32 CAGR: |

6.34% |

Market Size in 2032: |

USD 31.50 Billion |

|

Segments Covered: |

By Route of Administration |

|

|

|

By Application |

|

||

|

By End-use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Drug Delivery Device Market research report is 2024-2032.

Becton, Dickinson and Company (USA), Medtronic plc (Ireland), Johnson & Johnson (USA), Gerresheimer AG (Germany), Ypsomed Holding AG (Switzerland), West Pharmaceutical Services, Inc. (USA), Novo Nordisk A/S (Denmark), 3M Company (USA), Pfizer, Inc. (USA), Bayer AG (Germany), GlaxoSmithKline plc (UK), Sanofi S.A. (France), and Other Active Players

The Drug Delivery Device Market is segmented into Route of Administration, Application, End User and region. By Route of Administration, the market is categorized into Oral, Inhalation, Transdermal, Injectable, Ocular, Nasal, Topical, Others. By Application, the market is categorized into Oncology, Infectious Diseases, Respiratory Diseases, Diabetes, Cardiovascular Diseases, Autoimmune Diseases, Central Nervous System Disorders, Others. By End-use, the market is categorized into Hospitals, Diagnostic Centers, Ambulatory Surgery Centers/Clinics, Home Care Settings, Others. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, The Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC), Middle East & Africa (Turkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil, Argentina, Rest of SA).

The drug delivery device market comprises tools and technologies that are applied to deliver therapeutic agents to a patient in a controlled, efficient manner. Products include syringes, inhalers, transdermal patches, amongst many others; each product has helped facilitate targeted effective delivery of the medication. Product development is guided by the demand for enhanced patient outcomes, the reduction of side effects, and the optimization of bioavailability of drugs.

Drug Delivery Device Market Size Was Valued at USD 302.18 Billion in 2023, and is Projected to Reach USD 31.50 Billion by 2032, Growing at a CAGR of 6.34% From 2024-2032