Primary Packaging Market Synopsis:

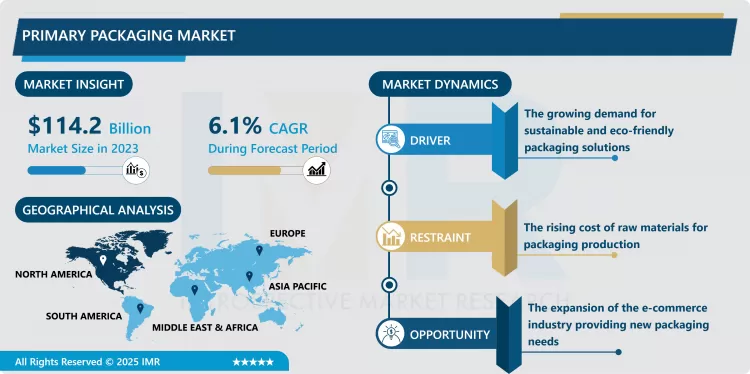

Primary Packaging Market Size Was Valued at USD 114.2 Billion in 2023, and is Projected to Reach USD 194.98 Billion by 2032, Growing at a CAGR of 6.1% From 2024-2032.

The primary packaging market has been defined as those packaging materials and systems that immediately surround, protect, contain, and sell a particular product. Primary packaging is to safeguard the products and their contents and integrity in several sectors such as medicine, food and beverages, beauty products, and medical products. Some of the main material that is employed in primary packaging include plastic and plastic derivatives such as PVC and PET, glass, metal tins and cans, paper and paper products; as well as many other composite and hybrid products, and its main function is to protect the commodity, make it easily manageable, and also help in marketing the product. Fluctuations of purchasing products at the global level have forced primary packaging market to develop rapidly particularly with reference to sustainable and recyclable materials along with a priority to convenience and appealing look.

The market for primary packaging has continue to grow significantly because of rising demand for better and strong packing material in different industries. In the food and beverage sector, primary packaging is particularly functional to preserve the quality of the product and extend its shelf life, so the market demand will be stimulated. Trends affecting packaging technologies have mainly being based on consumption habits of the society such as the convenience, portability, and the increasing awareness of the need for environmentally friendly packaging materials. Also, there has been massive awareness on the effects of packaging on the environment, thus the demand for multilayer and sustainable materials in the packing layers. Another major vehicle for the continued growth of this market is the pharmaceutical industry which entails compulsive safety and regulating measures. The primary packaging market is likely to grow at an accelerated pace due to developing new advanced technologies to its key subsegments such as smart packaging and active packaging.

Market is also driven by the factor such as online shopping and e-commerce through which the packaging solution that is more robust has gained importance. Customers are becoming more aware of the protection of their items through shipping hence the need to take packaging that will cater for the ferociousness of shipping and product Kahla (2011). In addition, sustainability is a major factor motivating the primary packaging industry because most industries have been forced to ensure that they minimize on the use of plastics and explore the use of green solutions. Government all over the world are pressing authorities in various regions to control packaging waste and paving the way towards sustainable packaging. One includes material that is reusable and recyclable, changes in packaging technology features as significant trends that will impact the market in the years ahead.

Primary Packaging Market Trend Analysis:

Sustainable Packaging Solutions

- Primary packaging changes Sustainability is rapidly becoming a key important factor when it comes to primary packaging changes. As the environment is a growing issue nowadays, companies are already searching for materials that can reduce the impact to the environment. More and more, customers are insisting on eco-friendly packaging, making businesses switch to reclosable, reusable, recyclable, biodegradable, and compostable materials. Manufacturers of packaging products are now coming up with new solution as they try to adopt the recycling of plastics, using plant based packaging material and minimizing packaging waste. In addition to considering the end of life of packaging, companies are also emphasizing on the total life cycle environmental cost of packaging or the entire carbon cost of packaging during production. To this effect, various forms of plastics from plants, biodegradable films with related tangible alternatives are fast becoming the world’s focal point when it comes to production.

Growth in E-Commerce Packaging

- Increase in the e-Commerce Packaging The e-commerce sector has experienced significant growth in the recent past; this makes it be an opportunity for the primary packaging market. By virtue of the growth in the need for online shopping, there is a growing need for proper compartments that are efficient, reliable, and well-protected to help in delivery of products in the best condition is paramount. Consumers and companies are likely to seek packaging techniques that can help them deliver their products safely in addition to creating some form of appeal as the market for electronic commerce continues to grow across the globe. Pressure from consumer for easy opening and disposal of packs and sheltering of product requirements during transportation has increased the market for innovative primary packaging. Furthermore, electronic commerce businesses are also incorporating environmentally sustainable packaging to help packaging companies to find new markets that embrace environmentally friendly packing solutions for their products.

Primary Packaging Market Segment Analysis:

Primary Packaging Market is Segmented on the basis of type, Mode of Packaging, Application, and Region

By Type, Clamshell Packaging segment is expected to dominate the market during the forecast period

- The clamshell packaging segment holds a noteworthy position in the global primary packaging market and is predicted to continue dominating over the market in the approaching forecast period due to rising usage across an exhaustive range of industries. Probably one of the reasons why clamshell packaging is quite popular among food and beverage industries, electronics, and retail stores is that clamshell packaging not only provides great protection for the products but also ensures that they remain easily visible. That is why the clamshell packaging allows holding products securely and offering the identifying signs of an attempt made to open it before, which is suitable for packing products that are expected to stay safe and easily noticeable at the same time. With more clamshell packaging being made from sustainable and recyclable material, further growth in the category is expected in the global market. With industries moving towards convenience packaging for consumers as well as being safety and environmentally friendly for products, clamshell packaging appears to be in the best position.

By Mode of Packaging, Boxes segment expected to held the largest share

- This research report expects that during the forecast period, the boxes segment will be occupying the largest market share of primary packaging. boxes give flexible, reusable, and cheap methods of packaging that can suit a broad range of products. Rising trends for strengthened packaging needs and secure transit requirements are also making the boxes segment a growth area. Boxes are especially popular in online store where they transport goods safely and systematically. Catering based on branding needs, the printed boxes make this type of packaging even more attractive to producers and manufactures. These remarkable appearances and more developments in the box manufacturing technologies and material have made the boxes segment to overly dominate the market.

Primary Packaging Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- According to the analysis, North America will continue to hold the largest share of the global primary packaging market in 2023, due to the several multinational packaging firms and latest technological developments in the region. This dominance is on account of the increasing utilization of primary packaging materials in the food and beverages, pharmaceuticals, and personal care products sectors. Also, the growth of sustainable packaging market is pushing the North American companies to invest more for the solutions. Since consumers are becoming more environmentally conscious and demanding recyclable materials for packaging, the North American Packaging manufacturers are among the foremost who have embraced and indeed invested on these biodegradable packing substances.

- North America owns the biggest market share and is supported by the growing eCommerce and online shopping, which directs to the need for robust and efficient packaging media for products’ shipment. This is in More so due to the region having strict laws regarding packaging especially in the food and drug industries hence the call for more quality packaging services. Increased strategic focus on innovation and sustainability in packaging across North America guarantees that the area remains the prime primary packaging market in the coming years.

Active Key Players in the Primary Packaging Market:

- Amcor (Australia)

- Ardagh Group (Ireland)

- Berry Global Inc. (USA)

- Crown Holdings Inc. (USA)

- DS Smith (UK)

- Eaton Corporation (Ireland)

- Global Closure Systems (France)

- Graphic Packaging International (USA)

- Huhtamaki Group (Finland)

- International Paper (USA)

- Mondi Group (Austria)

- Sealed Air Corporation (USA)

- Sonoco Products Company (USA)

- Tetra Pak (Sweden)

- WestRock Company (USA), and Other Active Players.

|

Global Primary Packaging Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 114.2 Billion |

|

Forecast Period 2024-32 CAGR: |

6.1% |

Market Size in 2032: |

USD 194.98 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Mode of Packaging |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Primary Packaging Market by By Type (2018-2032)

4.1 Primary Packaging Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Clamshell Packaging

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Blister Packs

4.5 Paperboard Packaging

4.6 Unit Dose Packs

4.7 Shrink-Wrapping

4.8 Others

Chapter 5: Primary Packaging Market by By Mode of Packaging (2018-2032)

5.1 Primary Packaging Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Boxes

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Cartons

5.5 Wrappers

5.6 Containers

5.7 Others

Chapter 6: Primary Packaging Market by By Application (2018-2032)

6.1 Primary Packaging Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Food and Beverages

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Pharmaceutical

6.5 Personal Care

6.6 Household Care

6.7 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Primary Packaging Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 AMCOR (AUSTRALIA)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 ARDAGH GROUP (IRELAND)

7.4 BERRY GLOBAL INC. (USA)

7.5 CROWN HOLDINGS INC. (USA)

7.6 DS SMITH (UK)

7.7 EATON CORPORATION (IRELAND)

7.8 GLOBAL CLOSURE SYSTEMS (FRANCE)

7.9 GRAPHIC PACKAGING INTERNATIONAL (USA)

7.10 HUHTAMAKI GROUP (FINLAND)

7.11 INTERNATIONAL PAPER (USA)

7.12 MONDI GROUP (AUSTRIA)

7.13 SEALED AIR CORPORATION (USA)

7.14 SONOCO PRODUCTS COMPANY (USA)

7.15 TETRA PAK (SWEDEN)

7.16 WESTROCK COMPANY (USA)

7.17 OTHER ACTIVE PLAYERS

Chapter 8: Global Primary Packaging Market By Region

8.1 Overview

8.2. North America Primary Packaging Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By By Type

8.2.4.1 Clamshell Packaging

8.2.4.2 Blister Packs

8.2.4.3 Paperboard Packaging

8.2.4.4 Unit Dose Packs

8.2.4.5 Shrink-Wrapping

8.2.4.6 Others

8.2.5 Historic and Forecasted Market Size By By Mode of Packaging

8.2.5.1 Boxes

8.2.5.2 Cartons

8.2.5.3 Wrappers

8.2.5.4 Containers

8.2.5.5 Others

8.2.6 Historic and Forecasted Market Size By By Application

8.2.6.1 Food and Beverages

8.2.6.2 Pharmaceutical

8.2.6.3 Personal Care

8.2.6.4 Household Care

8.2.6.5 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Primary Packaging Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By By Type

8.3.4.1 Clamshell Packaging

8.3.4.2 Blister Packs

8.3.4.3 Paperboard Packaging

8.3.4.4 Unit Dose Packs

8.3.4.5 Shrink-Wrapping

8.3.4.6 Others

8.3.5 Historic and Forecasted Market Size By By Mode of Packaging

8.3.5.1 Boxes

8.3.5.2 Cartons

8.3.5.3 Wrappers

8.3.5.4 Containers

8.3.5.5 Others

8.3.6 Historic and Forecasted Market Size By By Application

8.3.6.1 Food and Beverages

8.3.6.2 Pharmaceutical

8.3.6.3 Personal Care

8.3.6.4 Household Care

8.3.6.5 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Primary Packaging Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By By Type

8.4.4.1 Clamshell Packaging

8.4.4.2 Blister Packs

8.4.4.3 Paperboard Packaging

8.4.4.4 Unit Dose Packs

8.4.4.5 Shrink-Wrapping

8.4.4.6 Others

8.4.5 Historic and Forecasted Market Size By By Mode of Packaging

8.4.5.1 Boxes

8.4.5.2 Cartons

8.4.5.3 Wrappers

8.4.5.4 Containers

8.4.5.5 Others

8.4.6 Historic and Forecasted Market Size By By Application

8.4.6.1 Food and Beverages

8.4.6.2 Pharmaceutical

8.4.6.3 Personal Care

8.4.6.4 Household Care

8.4.6.5 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Primary Packaging Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By By Type

8.5.4.1 Clamshell Packaging

8.5.4.2 Blister Packs

8.5.4.3 Paperboard Packaging

8.5.4.4 Unit Dose Packs

8.5.4.5 Shrink-Wrapping

8.5.4.6 Others

8.5.5 Historic and Forecasted Market Size By By Mode of Packaging

8.5.5.1 Boxes

8.5.5.2 Cartons

8.5.5.3 Wrappers

8.5.5.4 Containers

8.5.5.5 Others

8.5.6 Historic and Forecasted Market Size By By Application

8.5.6.1 Food and Beverages

8.5.6.2 Pharmaceutical

8.5.6.3 Personal Care

8.5.6.4 Household Care

8.5.6.5 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Primary Packaging Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By By Type

8.6.4.1 Clamshell Packaging

8.6.4.2 Blister Packs

8.6.4.3 Paperboard Packaging

8.6.4.4 Unit Dose Packs

8.6.4.5 Shrink-Wrapping

8.6.4.6 Others

8.6.5 Historic and Forecasted Market Size By By Mode of Packaging

8.6.5.1 Boxes

8.6.5.2 Cartons

8.6.5.3 Wrappers

8.6.5.4 Containers

8.6.5.5 Others

8.6.6 Historic and Forecasted Market Size By By Application

8.6.6.1 Food and Beverages

8.6.6.2 Pharmaceutical

8.6.6.3 Personal Care

8.6.6.4 Household Care

8.6.6.5 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Primary Packaging Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By By Type

8.7.4.1 Clamshell Packaging

8.7.4.2 Blister Packs

8.7.4.3 Paperboard Packaging

8.7.4.4 Unit Dose Packs

8.7.4.5 Shrink-Wrapping

8.7.4.6 Others

8.7.5 Historic and Forecasted Market Size By By Mode of Packaging

8.7.5.1 Boxes

8.7.5.2 Cartons

8.7.5.3 Wrappers

8.7.5.4 Containers

8.7.5.5 Others

8.7.6 Historic and Forecasted Market Size By By Application

8.7.6.1 Food and Beverages

8.7.6.2 Pharmaceutical

8.7.6.3 Personal Care

8.7.6.4 Household Care

8.7.6.5 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Primary Packaging Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 114.2 Billion |

|

Forecast Period 2024-32 CAGR: |

6.1% |

Market Size in 2032: |

USD 194.98 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Mode of Packaging |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Primary Packaging Market research report is 2024-2032.

Amcor (Australia), Ardagh Group (Ireland), Berry Global Inc. (USA), Crown Holdings Inc. (USA), DS Smith (UK), Eaton Corporation (Ireland), Global Closure Systems (France), Graphic Packaging International (USA), Huhtamaki Group (Finland), International Paper (USA), Mondi Group (Austria), Sealed Air Corporation (USA), Sonoco Products Company (USA), Tetra Pak (Sweden), WestRock Company (USA), and Other Active Players.

The Primary Packaging Market is segmented into Type, Mode of Packaging, Application and region. By Type, the market is categorized into Clamshell Packaging, Blister Packs, Paperboard Packaging, Unit Dose Packs, Shrink-Wrapping, Others. By Mode of Packaging, the market is categorized into Boxes, Cartons, Wrappers, Containers, Others. By Application, the market is categorized into Food and Beverages, Pharmaceutical, Personal Care, Household Care, Others. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, The Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC), Middle East & Africa (Turkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil, Argentina, Rest of SA).

The primary packaging market has been defined as those packaging materials and systems that immediately surround, protect, contain, and sell a particular product. Primary packaging is to safeguard the products and their contents and integrity in several sectors such as medicine, food and beverages, beauty products, and medical products. Some of the main material that is employed in primary packaging include plastic and plastic derivatives such as PVC and PET, glass, metal tins and cans, paper and paper products; as well as many other composite and hybrid products, and its main function is to protect the commodity, make it easily manageable, and also help in marketing the product. Fluctuations of purchasing products at the global level have forced primary packaging market to develop rapidly particularly with reference to sustainable and recyclable materials along with a priority to convenience and appealing look.

Primary Packaging Market Size Was Valued at USD 114.2 Billion in 2023, and is Projected to Reach USD 194.98 Billion by 2032, Growing at a CAGR of 6.1% From 2024-2032.