Reverse Logistics Market Synopsis

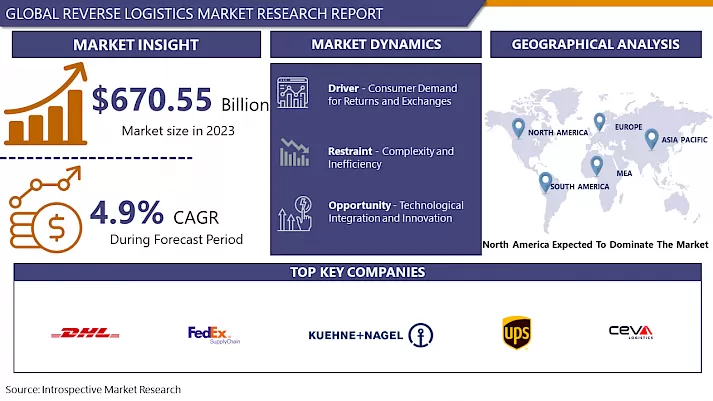

Reverse Logistics Market Size Was Valued at USD 670.55 Billion in 2023, and is Projected to Reach USD 1031.36 Billion by 2032, Growing at a CAGR of 4.9% From 2024-2032.

Reverse logistics, or reverse distribution, is the stage in the supply chain where a product is returned from the store to the manufacturer or distributor for reuse, repair, recycling or disposal.

- Reverse logistics refers to the supply chain process of returning items from end users back through the supply chain to either the retailer or producer. Whether the client is returning things they do not require, the end of the item life cycle has been come to or the item is harmed or flawed, it's basically great trade to offer returns to your clients, and that's where reverse logistics comes into play. This prepare moreover applies when things ought to be either arranged of or reused and incorporates the scenario where the conclusion client is the one dealing with the restoration, transfer or indeed resale of the item in question.

- The most common reverse-logistics prepare, returns management, deals with customary client returns and ought to represent a consistent, hassle-free involvement in arrange to boost client dependability and brand picture. Reconditioning items that are returned avoids organizations and retailers from forfeiting profit (or losing cash) on flawed items whereas dispensing with unnecessary waste.

- Some items need to be returned at the conclusion of their valuable life in arrange for producers to oversee their appropriate natural transfer. Organizations with bundling management forms are able to reuse bundling in arrange to decrease waste and spare the fetched that would something else be went through on unused bundling for returned things.

Reverse Lgistics Market Trend Analysis

Consumer Demand for Returns and Exchanges

- The blast of e-commerce has changed consumer shopping behaviour’s, coming about in a marked increment in item returns. Not at all like conventional retail, where clients can physically look at items some time recently buy, online customers frequently depend on depictions and pictures, driving to higher occurrences of disappointment and returns. This surge in e-commerce action has set exceptional requests on invert coordination’s frameworks. Moreover, advanced buyers anticipate consistent and adaptable return arrangements as a standard portion of their shopping encounter.

- They esteem the comfort of hassle-free returns, trades, and discounts, which are progressively getting to be unequivocal variables in their acquiring choices. Thus, retailers must contribute in vigorous invert coordination’s capabilities to oversee the tall volume of returns productively. This includes not as it were dealing with the coordination of moving items back through the supply chain but too guaranteeing that the method is cost-effective and customer-friendly. Compelling turn around coordination frameworks can upgrade client fulfilment, cultivate devotion, and separate a brand in a competitive showcase, whereas moreover contributing to supportability endeavours by guaranteeing returned items are suitably reused, repaired, or reused.

Opportunity

Technological Integration and Innovation

- Technological integration and development are revolutionizing turn around coordination, making forms more proficient and solid. Progressed advances like artificial intelligence (AI) and machine learning are being utilized to optimize different perspectives of turn around coordination, from foreseeing return designs to mechanizing sorting and handling errands. AI calculations can analyse huge datasets to recognize patterns in item returns, making a difference companies figure request for repairing or reusing operations. Machine learning can improve decision-making by distinguishing the foremost effective courses for returned products, decreasing transportation costs and natural affect.

- Blockchain innovation includes another layer of proficiency and transparency by giving a secure and unchanging record for following items all through the turn around coordination chain. This innovation guarantees that each exchange and development of products is recorded, upgrading traceability and decreasing the hazard of extortion. Blockchain can moreover streamline the coordination between distinctive partners, such as producers, retailers, and coordination suppliers, guaranteeing that returned items are handled rapidly and precisely. The improvement of smart return frameworks and computerized preparing offices encourage improves turn around coordination. Shrewd return frameworks permit clients to start returns online, get real-time upgrades, and select helpful drop-off or pickup alternatives. Robotized preparing offices utilize robotics and progressed sorting advances to handle returns productively, decreasing manual labour and preparing time. These offices can rapidly assess, sort, and course returned things to their fitting goals, whether for resale, restoration, or reusing. By and large, the integration of these progressed advances in switch coordination not as it were progresses operational proficiency and decreases costs but too improves client fulfilment by giving speedier and more dependable return administrations.

Reverse Logistics Market Segment Analysis:

Reverse Logistics market is segmented on the basis of Type, Service, Industry and Region

By Service, Transport Segment Is Expected to Dominate the Market During the Forecast Period

By Service it is segmented as Transportation, Warehousing, Reselling, Replacement Management, Refund Management, And Others.

- Transportation plays an essential part in switch logistics due to a few key variables that emphasize its dominance. Firstly, the volume and recurrence of returns, especially within the booming e-commerce division, require steady and productive development of goods from clients back to retailers, dissemination centers, or reusing offices. This continuous request for transportation administrations highlights its crucial significance. Also, the geographical spread of returns, which frequently include long separations and international courses, requires vigorous transportation systems to oversee the wide dispersion of clients and return handling areas viably. Transportation also speaks to a critical parcel of the generally fetched in invert logistics, making the optimization of courses and strategies basic for taken a toll administration.

- The time affectability of returns encourage intensifies the significance of proficient transportation, as speedy dealing with of returns is vital for keeping up client fulfilment and overseeing stock viably. Quick transportation guarantees that returned things are prepared quickly, whether for restocking, resale, or transfer, hence improving the in general effectiveness of invert logistics operations.

- Transportation is complicatedly connected with other turn around logistics administrations such as warehousing and substitution administration. Successful transportation systems empower consistent integration between these administrations, guaranteeing smooth and cohesive operations all through the turn around logistics chain. This interconnecting underscore transportation’s central part in keeping up a proficient and responsive invert logistics framework.

By Industry, Retail & E-commerce Segment Held the Largest Share In 2023

By Industry it is segmented as Retail & E-commerce, Automotive, Consumer Electronics, Healthcare, Food and Beverages, And Others.

- The retail and e-commerce division rules switch logistics essentially due to the high volume of returns inalienable in online shopping. Clients habitually buy different things with the purposeful of returning a few, driven by the failure to physically assess items some time recently buy. This leads to essentially higher return rates compared to conventional brick-and-mortar stores. Additionally, modern customers anticipate adaptable and hassle-free return approaches, compelling retailers to offer simple return alternatives to meet client desires and remain competitive.

- The segment moreover encounters significant surges in return volumes amid crest shopping seasons, such as occasions and deals occasions, requiring well-established invert logistics forms to oversee these vacillations proficiently. The differing extends of items sold—from clothing and embellishments to hardware and domestic goods—requires a flexible and versatile reverse logistics framework, as each item sort may have diverse return, restoration, and resale forms.

- The retail and e-commerce industry leverages progressed advances like AI, machine learning, and information analytics to improve turn around logistics. These innovations help in predicting return designs, optimizing stock administration, and moving forward client benefit. The worldwide reach of e-commerce includes another layer of complexity, requiring switch logistics systems competent of dealing with universal returns proficiently. These components collectively emphasize the retail and e-commerce sector's dominance in turn around logistics, driven by the got to oversee tall volumes, meet buyer desires, handle regular surges, oblige different item sorts, integrate progressed innovations, and oversee a global customer base.

- 2023 U.S. holiday sales are expected to increase by 4% year-over-year to a record $957.3 billion, according to the National Retail Federation (NRF), with 18% or $173 billion worth of returns. How efficiently these goods are added back to the supply chain through a process known as reverse logistics is a prime consideration for retailers from both a cost and environmental-impact perspective.

Reverse Logistics Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America is right now driving the invert logistics advertise due to a combination of a few compelling components. The locale gloats a develop e-commerce showcase, especially within the United States, where the tall infiltration of online shopping produces a noteworthy volume of returns, necessitating advanced invert logistics solutions. Buyer behaviour in North America encourage drives this request, as clients expect helpful and adaptable return arrangements. To meet these tall desires and stay competitive, retailers contribute to vigorous turn around logistics systems.

- Furthermore, North America is at the bleeding edge of technological innovation, with broad selection of progressed innovations like AI, machine learning, and blockchain. These technologies improve the productivity and viability of overseeing returns.

- The regulatory environment in North America underpins sustainable hones and productive squander administration, advancing advanced reverse logistics forms. Significant investment in logistics foundation and innovation moreover plays a crucial part, enabling the advancement of progressed frameworks to handle the high volume of returns more effectively. The region's well-established logistics and transportation systems encourage the smooth development of returned merchandise, advance improving operational proficiency.

- In addition, North America is home to retail mammoths such as Amazon and Walmart, whose significant assets and scale permit them to contribute intensely in turn around logistics, setting industry guidelines and driving showcase growth. Collectively, these variables make an ideal environment for compelling turn around logistics operations, setting North America's dominance in this market.

Reverse Logistics Market Active Players

- DHL Supply Chain (Germany)

- FedEx Supply Chain (United States)

- United Parcel Service (UPS) (United States)

- CEVA Logistics (France)

- Kuehne + Nagel (Switzerland)

- XPO Logistics (United States)

- Ryder System, Inc. (United States)

- Yusen Logistics (Japan)

- DB Schenker (Germany)

- GEODIS (France)

- SNCF Logistics (France)

- C.H. Robinson Worldwide, Inc. (United States)

- Kintetsu World Express (Japan)

- Nippon Express (Japan)

- DSV Panalpina (Denmark)

- Sinotrans Limited (China)

- Toll Group (Australia)

- J.B. Hunt Transport Services (United States)

- Menlo Worldwide Logistics (United States)

- Agility Logistics (Kuwait)

- Hellmann Worldwide Logistics (Germany)

- Penske Logistics (United States)

- Expeditors International (United States)

- A.P. Moller - Maersk (Denmark)

-

Global Reverse Logistics Market Scope:

Global Reverse Logistics Market

Base Year:

2023

Forecast Period:

2024-2032

Historical Data:

2017 to 2023

Market Size in 2023:

USD 670.55 Bn.

Forecast Period 2024-32 CAGR:

4.9 %

Market Size in 2032:

USD 1031.36 Bn.

Segments Covered:

By Type

- Recall Returns

- B2B Returns and Commercial Returns

- Repairable Returns

- End of Use Returns

- End of Life Returns

By Service

- Transportation

- Warehousing

- Reselling

- Replacement Management

- Refund Management

- Others

By Industry

- Retail & E-commerce

- Automotive

- Consumer Electronics

- Healthcare

- Food and Beverages

- Others

By Region

- North America (U.S., Canada, Mexico)

- Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

- Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

- Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC)

- Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

- South America (Brazil, Argentina, Rest of SA)

Key Market Drivers:

- Consumer Demand for Returns and Exchanges

Key Market Restraints:

- Complexity and Inefficiency

Key Opportunities:

- Technological Integration and Innovation

Companies Covered in the report:

- DHL Supply Chain (Germany), FedEx Supply Chain (United States), United Parcel Service (UPS) (United States), CEVA Logistics (France), Kuehne + Nagel (Switzerland) and Other Active Players.

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Reverse Logistics Market by By Type (2018-2032)

4.1 Reverse Logistics Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Recall Returns

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 B2B Returns and Commercial Returns

4.5 Repairable Returns

4.6 End of Use Returns

4.7 End of Life Returns

Chapter 5: Reverse Logistics Market by By Service (2018-2032)

5.1 Reverse Logistics Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Transportation

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Warehousing

5.5 Reselling

5.6 Replacement Management

5.7 Refund Management

5.8 Others

Chapter 6: Reverse Logistics Market by By Industry (2018-2032)

6.1 Reverse Logistics Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Retail & E-commerce

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Automotive

6.5 Consumer Electronics

6.6 Healthcare

6.7 Food and Beverages

6.8 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Reverse Logistics Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 DHL SUPPLY CHAIN (GERMANY)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 FEDEX SUPPLY CHAIN (UNITED STATES)

7.4 UNITED PARCEL SERVICE (UPS) (UNITED STATES)

7.5 CEVA LOGISTICS (FRANCE)

7.6 KUEHNE + NAGEL (SWITZERLAND)

7.7 XPO LOGISTICS (UNITED STATES)

7.8 RYDER SYSTEM INC. (UNITED STATES)

7.9 YUSEN LOGISTICS (JAPAN)

7.10 DB SCHENKER (GERMANY)

7.11 GEODIS (FRANCE)

7.12 SNCF LOGISTICS (FRANCE)

7.13 C.H. ROBINSON WORLDWIDE INC. (UNITED STATES)

7.14 KINTETSU WORLD EXPRESS (JAPAN)

7.15 NIPPON EXPRESS (JAPAN)

7.16 DSV PANALPINA (DENMARK)

7.17 SINOTRANS LIMITED (CHINA)

7.18 TOLL GROUP (AUSTRALIA)

7.19 J.B. HUNT TRANSPORT SERVICES (UNITED STATES)

7.20 MENLO WORLDWIDE LOGISTICS (UNITED STATES)

7.21 AGILITY LOGISTICS (KUWAIT)

7.22 HELLMANN WORLDWIDE LOGISTICS (GERMANY)

7.23 PENSKE LOGISTICS (UNITED STATES)

7.24 EXPEDITORS INTERNATIONAL (UNITED STATES)

7.25 A.P. MOLLER - MAERSK (DENMARK)

7.26 AIT WORLDWIDE LOGISTICS (UNITED STATES)

Chapter 8: Global Reverse Logistics Market By Region

8.1 Overview

8.2. North America Reverse Logistics Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By By Type

8.2.4.1 Recall Returns

8.2.4.2 B2B Returns and Commercial Returns

8.2.4.3 Repairable Returns

8.2.4.4 End of Use Returns

8.2.4.5 End of Life Returns

8.2.5 Historic and Forecasted Market Size By By Service

8.2.5.1 Transportation

8.2.5.2 Warehousing

8.2.5.3 Reselling

8.2.5.4 Replacement Management

8.2.5.5 Refund Management

8.2.5.6 Others

8.2.6 Historic and Forecasted Market Size By By Industry

8.2.6.1 Retail & E-commerce

8.2.6.2 Automotive

8.2.6.3 Consumer Electronics

8.2.6.4 Healthcare

8.2.6.5 Food and Beverages

8.2.6.6 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Reverse Logistics Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By By Type

8.3.4.1 Recall Returns

8.3.4.2 B2B Returns and Commercial Returns

8.3.4.3 Repairable Returns

8.3.4.4 End of Use Returns

8.3.4.5 End of Life Returns

8.3.5 Historic and Forecasted Market Size By By Service

8.3.5.1 Transportation

8.3.5.2 Warehousing

8.3.5.3 Reselling

8.3.5.4 Replacement Management

8.3.5.5 Refund Management

8.3.5.6 Others

8.3.6 Historic and Forecasted Market Size By By Industry

8.3.6.1 Retail & E-commerce

8.3.6.2 Automotive

8.3.6.3 Consumer Electronics

8.3.6.4 Healthcare

8.3.6.5 Food and Beverages

8.3.6.6 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Reverse Logistics Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By By Type

8.4.4.1 Recall Returns

8.4.4.2 B2B Returns and Commercial Returns

8.4.4.3 Repairable Returns

8.4.4.4 End of Use Returns

8.4.4.5 End of Life Returns

8.4.5 Historic and Forecasted Market Size By By Service

8.4.5.1 Transportation

8.4.5.2 Warehousing

8.4.5.3 Reselling

8.4.5.4 Replacement Management

8.4.5.5 Refund Management

8.4.5.6 Others

8.4.6 Historic and Forecasted Market Size By By Industry

8.4.6.1 Retail & E-commerce

8.4.6.2 Automotive

8.4.6.3 Consumer Electronics

8.4.6.4 Healthcare

8.4.6.5 Food and Beverages

8.4.6.6 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Reverse Logistics Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By By Type

8.5.4.1 Recall Returns

8.5.4.2 B2B Returns and Commercial Returns

8.5.4.3 Repairable Returns

8.5.4.4 End of Use Returns

8.5.4.5 End of Life Returns

8.5.5 Historic and Forecasted Market Size By By Service

8.5.5.1 Transportation

8.5.5.2 Warehousing

8.5.5.3 Reselling

8.5.5.4 Replacement Management

8.5.5.5 Refund Management

8.5.5.6 Others

8.5.6 Historic and Forecasted Market Size By By Industry

8.5.6.1 Retail & E-commerce

8.5.6.2 Automotive

8.5.6.3 Consumer Electronics

8.5.6.4 Healthcare

8.5.6.5 Food and Beverages

8.5.6.6 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Reverse Logistics Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By By Type

8.6.4.1 Recall Returns

8.6.4.2 B2B Returns and Commercial Returns

8.6.4.3 Repairable Returns

8.6.4.4 End of Use Returns

8.6.4.5 End of Life Returns

8.6.5 Historic and Forecasted Market Size By By Service

8.6.5.1 Transportation

8.6.5.2 Warehousing

8.6.5.3 Reselling

8.6.5.4 Replacement Management

8.6.5.5 Refund Management

8.6.5.6 Others

8.6.6 Historic and Forecasted Market Size By By Industry

8.6.6.1 Retail & E-commerce

8.6.6.2 Automotive

8.6.6.3 Consumer Electronics

8.6.6.4 Healthcare

8.6.6.5 Food and Beverages

8.6.6.6 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Reverse Logistics Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By By Type

8.7.4.1 Recall Returns

8.7.4.2 B2B Returns and Commercial Returns

8.7.4.3 Repairable Returns

8.7.4.4 End of Use Returns

8.7.4.5 End of Life Returns

8.7.5 Historic and Forecasted Market Size By By Service

8.7.5.1 Transportation

8.7.5.2 Warehousing

8.7.5.3 Reselling

8.7.5.4 Replacement Management

8.7.5.5 Refund Management

8.7.5.6 Others

8.7.6 Historic and Forecasted Market Size By By Industry

8.7.6.1 Retail & E-commerce

8.7.6.2 Automotive

8.7.6.3 Consumer Electronics

8.7.6.4 Healthcare

8.7.6.5 Food and Beverages

8.7.6.6 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

Global Reverse Logistics Market Scope:

|

Global Reverse Logistics Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 670.55 Bn. |

|

Forecast Period 2024-32 CAGR: |

4.9 % |

Market Size in 2032: |

USD 1031.36 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Service |

|

||

|

By Industry |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Reverse Logistics Market research report is 2024-2032.

DHL Supply Chain (Germany),FedEx Supply Chain (United States),United Parcel Service (UPS) (United States),CEVA Logistics (France),Kuehne + Nagel (Switzerland),XPO Logistics (United States),Ryder System, Inc. (United States),Yusen Logistics (Japan),DB Schenker (Germany),GEODIS (France),SNCF Logistics (France),C.H. Robinson Worldwide, Inc. (United States),Kintetsu World Express (Japan),Nippon Express (Japan),DSV Panalpina (Denmark),Sinotrans Limited (China),Toll Group (Australia),J.B. Hunt Transport Services (United States),Menlo Worldwide Logistics (United States),Agility Logistics (Kuwait),Hellmann Worldwide Logistics (Germany),Penske Logistics (United States),Expeditors International (United States),A.P. Moller - Maersk (Denmark),AIT Worldwide Logistics (United States) and Other Active Players.

The Reverse Logistics Market is segmented into Type, Service, Industry, Segment4, Segment5, Segment6, and region. By Type, the market is categorized into Recall Returns, B2B Returns and Commercial Returns, Repairable Returns, End of Use Returns, End of Life Returns. By Service, the market is categorized into Transportation, Warehousing, Reselling, Replacement Management, Refund Management, And Others. By Industry, the market is categorized into Retail & E-commerce, Automotive, Consumer Electronics, Healthcare, Food and Beverages, And Others. By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Reverse logistics, or reverse distribution, is the stage in the supply chain where a product is returned from the store to the manufacturer or distributor for reuse, repair, recycling or disposal.

Reverse Logistics Market Size Was Valued at USD 670.55 Billion in 2023, and is Projected to Reach USD 1031.36 Billion by 2032, Growing at a CAGR of 4.9% From 2024-2032.