Touch Screen Display Market Synopsis

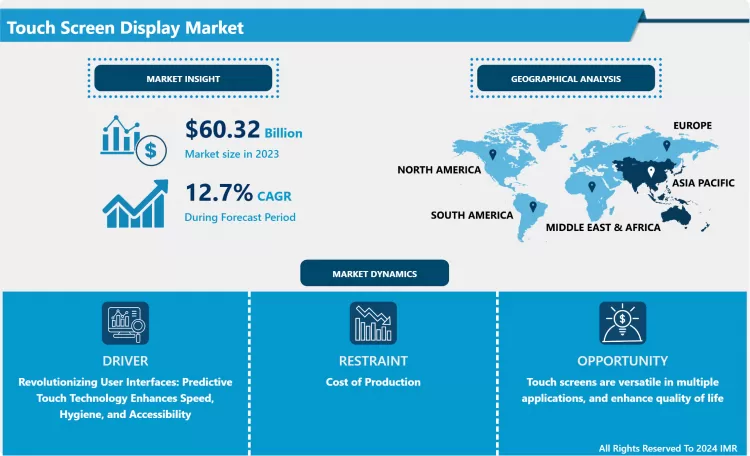

Touch Screen Display Market Size Was Valued at USD 60.32 Billion in 2023 and is Projected to Reach USD 176.92 Billion by 2032, Growing at a CAGR of 12.7% From 2024-2032.

A touchscreen (or touch screen) is a type of display that can detect touch input from a user. It consists of both an input device (a touch panel) and an output device (a visual display). The touch panel is typically layered on the top of the electronic visual display of a device. Touchscreens are commonly found in smartphones, tablets, laptops, and other electronic devices. The display is often an LCD, AMOLED, or OLED display.

- A user can give input or control the information processing system through simple or multi-touch gestures by touching the screen with a special stylus or one or more fingers. Some touchscreens use ordinary or specially coated gloves to work, while others may only work using a special stylus or pen. The user can use the touchscreen to react to what is displayed and, if the software allows, to control how it is displayed; for example, zooming to increase the text size.

- A touchscreen enables the user to interact directly with what is displayed, instead of using a mouse, touchpad, or other such devices (other than a stylus, which is optional for most modern touchscreens). Touchscreens are common in devices such as smartphones, handheld game consoles, and personal computers. They are common in point-of-sale (POS) systems, automated teller machines (ATMs), and electronic voting machines. They can also be attached to computers or, as terminals, to networks. They play a prominent role in the design of digital appliances such as personal digital assistants (PDAs) and some e-readers. Touchscreens are important in educational settings such as classrooms or on college campuses.

- The popularity of smartphones, tablets, and many types of information appliances has driven the demand and acceptance of common touchscreens for portable and functional electronics. Touchscreens are found in the medical field, heavy industry, automated teller machines (ATMs), and kiosks such as museum displays or room automation, where keyboard and mouse systems do not allow a suitably intuitive, rapid, or accurate interaction by the user with the display's content.

- Historically, the touchscreen sensor and its accompanying controller-based firmware have been made available by a wide array of after-market system integrators, and not by display, chip, or motherboard manufacturers. Display manufacturers and chip manufacturers have acknowledged the trend toward acceptance of touchscreens as a user interface component and have begun to integrate touchscreens into the fundamental design of their products.

Touch Screen Display Market Trend Analysis

Revolutionizing User Interfaces: Predictive Touch Technology Enhances Speed, Hygiene, and Accessibility.

- The innovative predictive touch technology developed by engineers from the University of Cambridge and Jaguar Land Rover is a new advancement in user interface technology. This system utilizes machine intelligence to forecast user actions through analyzing pointing processes, enabling quicker selection registration compared to conventional touch screens. Moreover, the technology also includes gesture-tracking features that utilize RF-based or vision-based sensors to recognize and analyze user gestures, improving precision and speed.

- Anticipatory touch technology provides flexibility on displays beyond regular touch screens, like holograms or projections. It supports inclusive design by adjusting to various user requirements and improving accessibility. In times of a pandemic, touchless interactions are vital for preventing the spread of viruses such as SARS-CoV-2 in public areas. The adaptability and personalization advantages of this technology benefit a variety of industries by offering creative solutions and enhancing user interactions, particularly for people with disabilities or challenges using standard touchscreens.

- Forecasting touch technology allows for easy integration into existing touch screen systems, converting them into touchless displays for rapid deployment across different industries. This new development improves public safety by decreasing physical interactions and potentially reducing the transmission of illnesses, especially in crowded places. The market is anticipated to undergo a major influence with the implementation and acceptance of this technology, as consumers and industries prioritize hygiene and efficiency. As predictive touch technology progresses, it paves the way for more advancements in user interfaces, possibly establishing new device design standards and transforming our daily interactions with technology.

Touch screens are versatile in multiple applications, and enhance quality of life.

- Jennifer Colegrove, who is the Vice President of emerging display technology at Display Search, asserts that the touchscreen industry is growing quickly, and is projected to double by 2017 and triple by 2022. Substituting ITO with alternative materials in touch technologies presents a significant opportunity by lowering expenses and allowing for the development of flexible electronics. Touch screens are becoming more common in eBooks, gaming systems, car dashboards, and other devices, as there is a rising need for slimmer, more lightweight, and less expensive screens. NPD Display Search forecasts that sensor-on-cover technology will be the top revenue generator in the market by 2015. Touch surfaces in the future will involve touchscreen video projectors, which will enable any surface to be interactive. Nevertheless, the touch market is challenging and unpredictable, as there is a risk of downturn due to decreased demand or the introduction of new technologies.

- Touch screens are very sustainable because of the vast amount of applications that can be done on one device. This can be seen very easily in the iPhone and Microsoft Surface. Before the iPhone, many people carried around a cell phone, iPod, and PDA. With the implementation of a versatile touch screen, the iPhone and other touchscreen devices can do the tasks of all three of these devices. This is because of the adaptability of the interface. The Microsoft Surface is similar to the iPhone because it makes many applications available to the user. Users can transfer contact information, calendars, pictures, etc. with just the touch of a finger. The sustainability aspects of both of these devices show the importance of these technologies.

- With the proliferation of low-cost, large-format displays, many customers are demanding to make these displays interactive. Typically, large-format displays range from 32 inches up to 82 inches. Public displays are intended for out-of-home viewing by multiple people. Touchscreen manufacturers have responded to meet this need in different ways. Some have chosen to develop purpose-built technologies specifically designed for large-format displays, while others have scaled up existing technologies to accommodate these larger sizes.

- Sustainability is the improvement of the quality of life by making life more enjoyable and less burdensome. Touchscreen technology fits within this definition very well. Touchscreen devices make life more enjoyable by creating a fun and intuitive user interface. This is a reason that the iPhone, iPod Touch, and similar devices are so successful. By allowing the user to operate the device in many different ways, the devices are more versatile and create a better interface for many applications. With a better interface, the devices become more enjoyable to use and allow for other applications on the device. Sustainability also pertains to making life less burdensome.

Touch Screen Display Market Segment Analysis:

Touch Screen Display Market Segmented based on Screen Type, Application, End-use, Display Type, Mounting Option, And Interaction Method.

By Screen Type, Capacitive Touch Screens Segment Is Expected to Dominate the Market During the Forecast Period

- Capacitive popularity has grown, as it has become one of the leading technologies used in touch screen devices. In 2001, it began appearing in consumer devices, such as MP3 players and smartphones. This increase in attention is likely due to the effectiveness of its design, its use of multi-touch technology, and the popularity of Apple products using this technology: iPod Touch, iPhone, and most recently the iPad.

- Capacitive touchscreen displays rely on the electrical properties of the human body to detect when and where on a display the user is touching. Because of this capacitive display can be controlled with very light touches of a finger, generally, they cannot be used with a mechanical stylus or a gloved hand. The most significant advantages of capacitive screens are their strength and durability. A touch screen will increasingly be used in business applications. In addition, dirt and fingerprint smudges do not impact the performance of a capacitive touch screen that has been carefully picked and developed.

- There are two types of capacitive touchscreen generally available, surface and projected, and it’s the latter that you’ll find in Apple's iPhone and iPod. The internal structures differ between the two types. They are both based on the fact that the application of a finger changes the capacitance in a local region enabling the system’s electronics to detect a touch and determine its position on the screen. Compared with resistive, capacitive systems detect changes in electrical fields but don't rely on pressure.

By Application, Consumer Electronics Segment Held the Largest Share In 2023

- Smartphones, in particular, are leading the way in the touch screen display market for consumer electronics. The rise is fueled by the growing need for smartphones and improvements in mobile technologies such as 5G and AI. Customers favor devices equipped with advanced touch screen technology, such as superior picture clarity and enhanced touch responsiveness. Consumers also prioritize features such as compact designs and long-lasting screens. In general, touch screen displays in consumer electronics are dominating the market share due to the variety of uses in this industry.

- The increase in popularity of hybrid laptops and tablets featuring touch screen displays satisfies the need for flexible devices for work and education. Touch-enabled smart TVs provide interactive entertainment and home automation, aligning with the trend for improved resolution screens. The demand for productivity features, interactive learning tools, and high-quality visuals in the age of remote work and online education is what fuels the popularity of these devices.

- The smart wearables market, such as fitness trackers and smartwatches, is growing rapidly, necessitating touch screens that are both responsive, long-lasting, and energy-efficient. Consumers desire wearables that have convenient access to information and seamless interaction, facilitated by advanced touch screen technology. Smartphones, tablets, and smart TVs have clear images on high-resolution touch screens, thanks to OLED and AMOLED technology providing excellent color and brightness. Touchscreen technology enables slim device aesthetics, full-screen displays, and versatility. They also decrease battery usage, provide lasting performance, and improve ease of use. The increasing need for cutting-edge touch screens is on the rise due to the growth of smart devices and ongoing technological advancements, addressing consumers' heightened dependence on mobile and smart technologies in communication, entertainment, work, and health tracking.

Touch Screen Display Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- Asia Pacific is the leading region in the touchscreen display market for various reasons. The area acts as a center for manufacturing, with leading manufacturers such as Samsung, LG, and Foxconn based in nations like China, South Korea, Japan, and Taiwan. The ability to produce large quantities and having established supply chains result in cost savings and increased production scale, leading to lower prices and global competitiveness of touchscreen displays. Moreover, the Asia Pacific region places a substantial focus on research and development, resulting in ongoing technological progress such as flexible displays and enhanced touch sensitivity. Both South Korea and Japan are well-known for their advanced research and development facilities.

- Utilizing modern manufacturing techniques like automation, robotics, and AI-driven processes enhances the quality and efficiency of producing touchscreen displays. The fast-economic development in nations such as China and India has resulted in the emergence of a larger middle class with more money to spend, resulting in a heightened interest for consumer electronics such as smartphones, tablets, and smart TVs. The younger population in the Asia Pacific area is very skilled with technology, leading to increased usage of the newest consumer gadgets. Asia Pacific is a major center for manufacturing consumer electronics, as local brands and OEMs are driving the market for touch screen devices in the region.

- Incentives and subsidies from governments in the Asia Pacific region, specifically in China and India, are provided to aid the electronics manufacturing sector. Through the adoption of initiatives like "Made in China 2025" and "Make in India," the goal is to increase domestic manufacturing capacity and allure foreign investments. Investments in developing infrastructure such as technology parks and industrial zones also contribute to the growth of the touch screen display market. Skilled yet affordable labor in countries such as China, India, and Vietnam lowers production expenses, making the area appealing for manufacturing. Prioritizing technical education leads to a consistent flow of skilled workers, enhancing the region's competitiveness in the global touch screen display market.

Touch Screen Display Market Active Players

- BOE Technology Group Co., Ltd. (China)

- Innolux Corporation (Taiwan)

- AU Optronics Corp. (Taiwan)

- Panasonic Holdings Corporation (Japan)

- Samsung Electronics (South Korea)

- Corning Incorporated (US)

- Mouser Electronics, Inc. (US)

- FUJITSU (Japan)

- NEC Corporation (Japan)

- DISPLAX (Portugal)

- Atmel Corporation (US)

- Microsoft Corporation (US)

- The 3M Company (US)

- American Industrial Systems Inc. (AIS) (US)

- LG Electronics (South Korea)

- Cypress Semiconductor Corporation (US)

- Synaptics Incorporated (US)

- WINTEK Corporation (US)

- Sharp Corporation (Japan)

- Qisda Corporation (Taiwan)

- AD Metro (Canada)

-

Global Touch Screen Display Market

Base Year:

2023

Forecast Period:

2024-2032

Historical Data:

2017 to 2023

Market Size in 2023:

USD 60.32 Bn.

Forecast Period 2024-32 CAGR:

12.7 %

Market Size in 2032:

USD 176.92 Bn.

Segments Covered:

By Screen Type

- Resistive Touch Screens

- Capacitive Touch Screens

- Infrared Touch Screens

- Optical

- Surface Acoustic Wave Type Displays

- Projected Capacitive Touch Screen (PCT or PCAP)

By Application

- Display/Digital Signage

- Kiosks

- Consumer Electronics {Laptops & Tablets and Smart Television, Smartphones & Smart Wearables}

By End-use

- Automotive

- Healthcare

- Retail

- Industrial

- Consumer Electronics

- Education

By Display Type

- LCD (Liquid Crystal Display)

- LED (Light Emitting Diode)

- OLED (Organic Light Emitting Diode)

- AMOLED (Active Matrix OLED)

By Mounting Option

- Wall-Mounted

- Tabletop

- Embedded/In-Built

By Interaction Method

- Touch-Based

- Pen/Stylus-Based

- Touchless (Gesture-Based)

By Region

- North America (U.S., Canada, Mexico)

- Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

- Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

- Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC)

- Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

- South America (Brazil, Argentina, Rest of SA)

Key Market Drivers:

- Revolutionizing User Interfaces: Predictive Touch Technology Enhances Speed, Hygiene, and Accessibility

Key Market Restraints:

- Cost of Production

Key Opportunities:

- Touch screens are versatile in multiple applications, and enhance quality of life

Companies Covered in the report:

- BOE Technology Group Co., Ltd. (China), Innolux Corporation (Taiwan), AU Optronics Corp. (Taiwan), Panasonic Holdings Corporation (Japan), Samsung Electronics (South Korea), Corning Incorporated (US), and Other Active Players.

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Touch Screen Display Market by By Screen Type (2018-2032)

4.1 Touch Screen Display Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Resistive Touch Screens

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Capacitive Touch Screens

4.5 Infrared Touch Screens

4.6 Optical

4.7 Surface Acoustic Wave Type Displays

4.8 Projected Capacitive Touch Screen (PCT or PCAP)

Chapter 5: Touch Screen Display Market by By Application (2018-2032)

5.1 Touch Screen Display Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Display/Digital Signage

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Kiosks

5.5 Consumer Electronics {Laptops & Tablets and Smart Television

5.6 Smartphones & Smart Wearables}

Chapter 6: Touch Screen Display Market by By End-use (2018-2032)

6.1 Touch Screen Display Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Automotive

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Healthcare

6.5 Retail

6.6 Industrial

6.7 Consumer Electronics

6.8 Education

Chapter 7: Touch Screen Display Market by By Display Type (2018-2032)

7.1 Touch Screen Display Market Snapshot and Growth Engine

7.2 Market Overview

7.3 LCD (Liquid Crystal Display)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 LED (Light Emitting Diode)

7.5 OLED (Organic Light Emitting Diode)

7.6 AMOLED (Active Matrix OLED)

Chapter 8: Touch Screen Display Market by By Mounting Option (2018-2032)

8.1 Touch Screen Display Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Wall-Mounted

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Tabletop

8.5 Embedded/In-Built

Chapter 9: Touch Screen Display Market by By Interaction Method (2018-2032)

9.1 Touch Screen Display Market Snapshot and Growth Engine

9.2 Market Overview

9.3 Touch-Based

9.3.1 Introduction and Market Overview

9.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

9.3.3 Key Market Trends, Growth Factors, and Opportunities

9.3.4 Geographic Segmentation Analysis

9.4 Pen/Stylus-Based

9.5 Touchless (Gesture-Based)

Chapter 10: Company Profiles and Competitive Analysis

10.1 Competitive Landscape

10.1.1 Competitive Benchmarking

10.1.2 Touch Screen Display Market Share by Manufacturer (2024)

10.1.3 Industry BCG Matrix

10.1.4 Heat Map Analysis

10.1.5 Mergers and Acquisitions

10.2 BOE TECHNOLOGY GROUP COLTD. (CHINA)

10.2.1 Company Overview

10.2.2 Key Executives

10.2.3 Company Snapshot

10.2.4 Role of the Company in the Market

10.2.5 Sustainability and Social Responsibility

10.2.6 Operating Business Segments

10.2.7 Product Portfolio

10.2.8 Business Performance

10.2.9 Key Strategic Moves and Recent Developments

10.2.10 SWOT Analysis

10.3 INNOLUX CORPORATION (TAIWAN)

10.4 AU OPTRONICS CORP. (TAIWAN)

10.5 PANASONIC HOLDINGS CORPORATION (JAPAN)

10.6 SAMSUNG ELECTRONICS (SOUTH KOREA)

10.7 CORNING INCORPORATED (US)

10.8 MOUSER ELECTRONICS INC. (US)

10.9 FUJITSU (JAPAN)

10.10 NEC CORPORATION (JAPAN)

10.11 DISPLAX (PORTUGAL)

10.12 ATMEL CORPORATION (US)

10.13 MICROSOFT CORPORATION (US)

10.14 THE 3M COMPANY (US)

10.15 AMERICAN INDUSTRIAL SYSTEMS INC. (AIS) (US)

10.16 LG ELECTRONICS (SOUTH KOREA)

10.17 CYPRESS SEMICONDUCTOR CORPORATION (US)

10.18 SYNAPTICS INCORPORATED (US)

10.19 WINTEK CORPORATION (US)

10.20 SHARP CORPORATION (JAPAN)

10.21 QISDA CORPORATION (TAIWAN)

10.22 AD METRO (CANADA)

10.23 TCL TECHNOLOGY (CHINA)

10.24 HANNSTAR DISPLAY CORPORATION (TAIWAN)

10.25 CHUNGHWA PICTURE TUBES LTD. (TAIWAN)

10.26 JAPAN DISPLAY INC. (JDI) (JAPAN)

10.27 TPK HOLDING COLTD. (TAIWAN)

10.28 UNIVERSAL DISPLAY CORPORATION (US)

10.29 ELO TOUCH SOLUTIONS (US)

10.30 WINTEK CORPORATION (TAIWAN)

10.31 TOUCH INTERNATIONAL (US)

10.32 MITSUBISHI ELECTRIC CORPORATION (JAPAN)

Chapter 11: Global Touch Screen Display Market By Region

11.1 Overview

11.2. North America Touch Screen Display Market

11.2.1 Key Market Trends, Growth Factors and Opportunities

11.2.2 Top Key Companies

11.2.3 Historic and Forecasted Market Size by Segments

11.2.4 Historic and Forecasted Market Size By By Screen Type

11.2.4.1 Resistive Touch Screens

11.2.4.2 Capacitive Touch Screens

11.2.4.3 Infrared Touch Screens

11.2.4.4 Optical

11.2.4.5 Surface Acoustic Wave Type Displays

11.2.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.2.5 Historic and Forecasted Market Size By By Application

11.2.5.1 Display/Digital Signage

11.2.5.2 Kiosks

11.2.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.2.5.4 Smartphones & Smart Wearables}

11.2.6 Historic and Forecasted Market Size By By End-use

11.2.6.1 Automotive

11.2.6.2 Healthcare

11.2.6.3 Retail

11.2.6.4 Industrial

11.2.6.5 Consumer Electronics

11.2.6.6 Education

11.2.7 Historic and Forecasted Market Size By By Display Type

11.2.7.1 LCD (Liquid Crystal Display)

11.2.7.2 LED (Light Emitting Diode)

11.2.7.3 OLED (Organic Light Emitting Diode)

11.2.7.4 AMOLED (Active Matrix OLED)

11.2.8 Historic and Forecasted Market Size By By Mounting Option

11.2.8.1 Wall-Mounted

11.2.8.2 Tabletop

11.2.8.3 Embedded/In-Built

11.2.9 Historic and Forecasted Market Size By By Interaction Method

11.2.9.1 Touch-Based

11.2.9.2 Pen/Stylus-Based

11.2.9.3 Touchless (Gesture-Based)

11.2.10 Historic and Forecast Market Size by Country

11.2.10.1 US

11.2.10.2 Canada

11.2.10.3 Mexico

11.3. Eastern Europe Touch Screen Display Market

11.3.1 Key Market Trends, Growth Factors and Opportunities

11.3.2 Top Key Companies

11.3.3 Historic and Forecasted Market Size by Segments

11.3.4 Historic and Forecasted Market Size By By Screen Type

11.3.4.1 Resistive Touch Screens

11.3.4.2 Capacitive Touch Screens

11.3.4.3 Infrared Touch Screens

11.3.4.4 Optical

11.3.4.5 Surface Acoustic Wave Type Displays

11.3.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.3.5 Historic and Forecasted Market Size By By Application

11.3.5.1 Display/Digital Signage

11.3.5.2 Kiosks

11.3.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.3.5.4 Smartphones & Smart Wearables}

11.3.6 Historic and Forecasted Market Size By By End-use

11.3.6.1 Automotive

11.3.6.2 Healthcare

11.3.6.3 Retail

11.3.6.4 Industrial

11.3.6.5 Consumer Electronics

11.3.6.6 Education

11.3.7 Historic and Forecasted Market Size By By Display Type

11.3.7.1 LCD (Liquid Crystal Display)

11.3.7.2 LED (Light Emitting Diode)

11.3.7.3 OLED (Organic Light Emitting Diode)

11.3.7.4 AMOLED (Active Matrix OLED)

11.3.8 Historic and Forecasted Market Size By By Mounting Option

11.3.8.1 Wall-Mounted

11.3.8.2 Tabletop

11.3.8.3 Embedded/In-Built

11.3.9 Historic and Forecasted Market Size By By Interaction Method

11.3.9.1 Touch-Based

11.3.9.2 Pen/Stylus-Based

11.3.9.3 Touchless (Gesture-Based)

11.3.10 Historic and Forecast Market Size by Country

11.3.10.1 Russia

11.3.10.2 Bulgaria

11.3.10.3 The Czech Republic

11.3.10.4 Hungary

11.3.10.5 Poland

11.3.10.6 Romania

11.3.10.7 Rest of Eastern Europe

11.4. Western Europe Touch Screen Display Market

11.4.1 Key Market Trends, Growth Factors and Opportunities

11.4.2 Top Key Companies

11.4.3 Historic and Forecasted Market Size by Segments

11.4.4 Historic and Forecasted Market Size By By Screen Type

11.4.4.1 Resistive Touch Screens

11.4.4.2 Capacitive Touch Screens

11.4.4.3 Infrared Touch Screens

11.4.4.4 Optical

11.4.4.5 Surface Acoustic Wave Type Displays

11.4.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.4.5 Historic and Forecasted Market Size By By Application

11.4.5.1 Display/Digital Signage

11.4.5.2 Kiosks

11.4.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.4.5.4 Smartphones & Smart Wearables}

11.4.6 Historic and Forecasted Market Size By By End-use

11.4.6.1 Automotive

11.4.6.2 Healthcare

11.4.6.3 Retail

11.4.6.4 Industrial

11.4.6.5 Consumer Electronics

11.4.6.6 Education

11.4.7 Historic and Forecasted Market Size By By Display Type

11.4.7.1 LCD (Liquid Crystal Display)

11.4.7.2 LED (Light Emitting Diode)

11.4.7.3 OLED (Organic Light Emitting Diode)

11.4.7.4 AMOLED (Active Matrix OLED)

11.4.8 Historic and Forecasted Market Size By By Mounting Option

11.4.8.1 Wall-Mounted

11.4.8.2 Tabletop

11.4.8.3 Embedded/In-Built

11.4.9 Historic and Forecasted Market Size By By Interaction Method

11.4.9.1 Touch-Based

11.4.9.2 Pen/Stylus-Based

11.4.9.3 Touchless (Gesture-Based)

11.4.10 Historic and Forecast Market Size by Country

11.4.10.1 Germany

11.4.10.2 UK

11.4.10.3 France

11.4.10.4 The Netherlands

11.4.10.5 Italy

11.4.10.6 Spain

11.4.10.7 Rest of Western Europe

11.5. Asia Pacific Touch Screen Display Market

11.5.1 Key Market Trends, Growth Factors and Opportunities

11.5.2 Top Key Companies

11.5.3 Historic and Forecasted Market Size by Segments

11.5.4 Historic and Forecasted Market Size By By Screen Type

11.5.4.1 Resistive Touch Screens

11.5.4.2 Capacitive Touch Screens

11.5.4.3 Infrared Touch Screens

11.5.4.4 Optical

11.5.4.5 Surface Acoustic Wave Type Displays

11.5.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.5.5 Historic and Forecasted Market Size By By Application

11.5.5.1 Display/Digital Signage

11.5.5.2 Kiosks

11.5.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.5.5.4 Smartphones & Smart Wearables}

11.5.6 Historic and Forecasted Market Size By By End-use

11.5.6.1 Automotive

11.5.6.2 Healthcare

11.5.6.3 Retail

11.5.6.4 Industrial

11.5.6.5 Consumer Electronics

11.5.6.6 Education

11.5.7 Historic and Forecasted Market Size By By Display Type

11.5.7.1 LCD (Liquid Crystal Display)

11.5.7.2 LED (Light Emitting Diode)

11.5.7.3 OLED (Organic Light Emitting Diode)

11.5.7.4 AMOLED (Active Matrix OLED)

11.5.8 Historic and Forecasted Market Size By By Mounting Option

11.5.8.1 Wall-Mounted

11.5.8.2 Tabletop

11.5.8.3 Embedded/In-Built

11.5.9 Historic and Forecasted Market Size By By Interaction Method

11.5.9.1 Touch-Based

11.5.9.2 Pen/Stylus-Based

11.5.9.3 Touchless (Gesture-Based)

11.5.10 Historic and Forecast Market Size by Country

11.5.10.1 China

11.5.10.2 India

11.5.10.3 Japan

11.5.10.4 South Korea

11.5.10.5 Malaysia

11.5.10.6 Thailand

11.5.10.7 Vietnam

11.5.10.8 The Philippines

11.5.10.9 Australia

11.5.10.10 New Zealand

11.5.10.11 Rest of APAC

11.6. Middle East & Africa Touch Screen Display Market

11.6.1 Key Market Trends, Growth Factors and Opportunities

11.6.2 Top Key Companies

11.6.3 Historic and Forecasted Market Size by Segments

11.6.4 Historic and Forecasted Market Size By By Screen Type

11.6.4.1 Resistive Touch Screens

11.6.4.2 Capacitive Touch Screens

11.6.4.3 Infrared Touch Screens

11.6.4.4 Optical

11.6.4.5 Surface Acoustic Wave Type Displays

11.6.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.6.5 Historic and Forecasted Market Size By By Application

11.6.5.1 Display/Digital Signage

11.6.5.2 Kiosks

11.6.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.6.5.4 Smartphones & Smart Wearables}

11.6.6 Historic and Forecasted Market Size By By End-use

11.6.6.1 Automotive

11.6.6.2 Healthcare

11.6.6.3 Retail

11.6.6.4 Industrial

11.6.6.5 Consumer Electronics

11.6.6.6 Education

11.6.7 Historic and Forecasted Market Size By By Display Type

11.6.7.1 LCD (Liquid Crystal Display)

11.6.7.2 LED (Light Emitting Diode)

11.6.7.3 OLED (Organic Light Emitting Diode)

11.6.7.4 AMOLED (Active Matrix OLED)

11.6.8 Historic and Forecasted Market Size By By Mounting Option

11.6.8.1 Wall-Mounted

11.6.8.2 Tabletop

11.6.8.3 Embedded/In-Built

11.6.9 Historic and Forecasted Market Size By By Interaction Method

11.6.9.1 Touch-Based

11.6.9.2 Pen/Stylus-Based

11.6.9.3 Touchless (Gesture-Based)

11.6.10 Historic and Forecast Market Size by Country

11.6.10.1 Turkiye

11.6.10.2 Bahrain

11.6.10.3 Kuwait

11.6.10.4 Saudi Arabia

11.6.10.5 Qatar

11.6.10.6 UAE

11.6.10.7 Israel

11.6.10.8 South Africa

11.7. South America Touch Screen Display Market

11.7.1 Key Market Trends, Growth Factors and Opportunities

11.7.2 Top Key Companies

11.7.3 Historic and Forecasted Market Size by Segments

11.7.4 Historic and Forecasted Market Size By By Screen Type

11.7.4.1 Resistive Touch Screens

11.7.4.2 Capacitive Touch Screens

11.7.4.3 Infrared Touch Screens

11.7.4.4 Optical

11.7.4.5 Surface Acoustic Wave Type Displays

11.7.4.6 Projected Capacitive Touch Screen (PCT or PCAP)

11.7.5 Historic and Forecasted Market Size By By Application

11.7.5.1 Display/Digital Signage

11.7.5.2 Kiosks

11.7.5.3 Consumer Electronics {Laptops & Tablets and Smart Television

11.7.5.4 Smartphones & Smart Wearables}

11.7.6 Historic and Forecasted Market Size By By End-use

11.7.6.1 Automotive

11.7.6.2 Healthcare

11.7.6.3 Retail

11.7.6.4 Industrial

11.7.6.5 Consumer Electronics

11.7.6.6 Education

11.7.7 Historic and Forecasted Market Size By By Display Type

11.7.7.1 LCD (Liquid Crystal Display)

11.7.7.2 LED (Light Emitting Diode)

11.7.7.3 OLED (Organic Light Emitting Diode)

11.7.7.4 AMOLED (Active Matrix OLED)

11.7.8 Historic and Forecasted Market Size By By Mounting Option

11.7.8.1 Wall-Mounted

11.7.8.2 Tabletop

11.7.8.3 Embedded/In-Built

11.7.9 Historic and Forecasted Market Size By By Interaction Method

11.7.9.1 Touch-Based

11.7.9.2 Pen/Stylus-Based

11.7.9.3 Touchless (Gesture-Based)

11.7.10 Historic and Forecast Market Size by Country

11.7.10.1 Brazil

11.7.10.2 Argentina

11.7.10.3 Rest of SA

Chapter 12 Analyst Viewpoint and Conclusion

12.1 Recommendations and Concluding Analysis

12.2 Potential Market Strategies

Chapter 13 Research Methodology

13.1 Research Process

13.2 Primary Research

13.3 Secondary Research

|

Global Touch Screen Display Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 60.32 Bn. |

|

Forecast Period 2024-32 CAGR: |

12.7 % |

Market Size in 2032: |

USD 176.92 Bn. |

|

Segments Covered: |

By Screen Type |

|

|

|

By Application |

|

||

|

By End-use |

|

||

|

By Display Type |

|

||

|

By Mounting Option |

|

||

|

By Interaction Method |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Touch Screen Display Market research report is 2024-2032.

BOE Technology Group Co., Ltd. (China), Innolux Corporation (Taiwan), AU Optronics Corp. (Taiwan), Panasonic Holdings Corporation (Japan), Samsung Electronics (South Korea), Corning Incorporated (US), Mouser Electronics, Inc. (US),FUJITSU (Japan), NEC Corporation (Japan),DISPLAX (Portugal), Atmel Corporation (US), Microsoft Corporation (US), The 3M Company (US), American Industrial Systems Inc. (AIS) (US), LG Electronics (South Korea),Cypress Semiconductor Corporation (US), Synaptics Incorporated (US), WINTEK Corporation (US), Sharp Corporation (Japan), Qisda Corporation (Taiwan), AD Metro (Canada), TCL Technology (China), HannStar Display Corporation (Taiwan), Chunghwa Picture Tubes Ltd. (Taiwan), Japan Display Inc. (JDI) (Japan), TPK Holding Co., Ltd. (Taiwan), Universal Display Corporation (US), ELO Touch Solutions (US), Wintek Corporation (Taiwan), Touch International (US), Mitsubishi Electric Corporation (Japan) and Other Active Players.

The Touch Screen Display Market is segmented into Screen Type, Application, End-use, Display Type, Mounting Option, Interaction Method, and Region. By Screen Type, the market is categorized into Resistive Touch Screens, Capacitive Touch Screens, Infrared Touch Screens, Optical, Surface Acoustic Wave Type Displays, And Projected Capacitive Touch Screen (PCT or PCAP). By Application, the market is categorized into Display/Digital Signage, Kiosks, Consumer Electronics {Laptops & Tablets and Smart Television, Smartphones & Smart Wearables}. By End-use, the market is categorized into Automotive, Healthcare, Retail, Industrial, Consumer Electronics, And Education. By Display Type, the market is categorized into LCD (Liquid Crystal Display), LED (Light Emitting Diode), OLED (Organic Light Emitting Diode), and AMOLED (Active Matrix OLED). By Mounting Option, The Market Is Categorized Into Wall-Mounted, Tabletop, and Embedded/In-Built. By Interaction Method, the market is categorized into Touch-Based, Pen/Stylus-Based, Touchless (Gesture-Based), Interaction Method, and Interaction. By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

A touchscreen (or touch screen) is a type of display that can detect touch input from a user. It consists of both an input device (a touch panel) and an output device (a visual display). The touch panel is typically layered on the top of the electronic visual display of a device. Touchscreens are commonly found in smartphones, tablets, laptops, and other electronic devices. The display is often an LCD, AMOLED, or OLED display.

Touch Screen Display Market Size Was Valued at USD 60.32 Billion in 2023, and is Projected to Reach USD 176.92 Billion by 2032, Growing at a CAGR of 12.7% From 2024-2032.